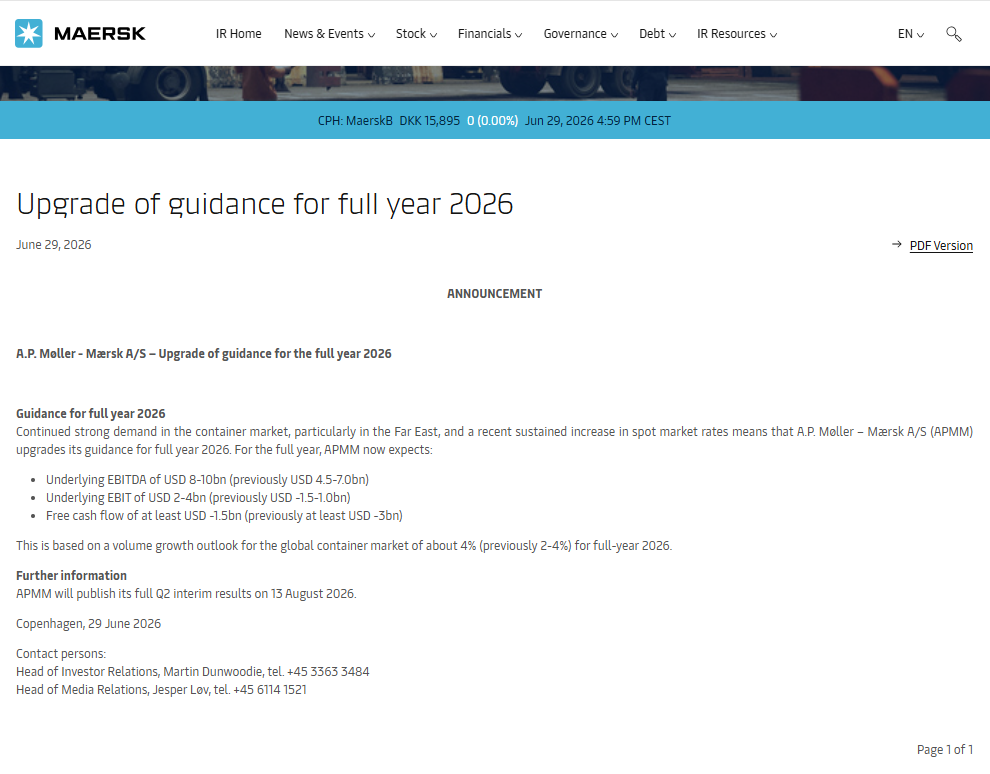

Maersk Lifts 2026 Guidance by Up to $3.5bn as Container Market Turns More Profitable

Xinde Marine News — A.P. Møller - Mærsk has sharply upgraded its full-year 2026 earnings guidance, in one of the clearest signs yet that the container shipping market is performing better than expected.

Strong Far East demand, rising spot rates and persistent supply chain disruption are reshaping liner earnings expectations

The revision, announced in Copenhagen on 29 June, came less than two months after Maersk reported its first-quarter results and issued its previous full-year outlook.

The change is significant.

Maersk now expects underlying EBITDA of $8bn to $10bn for 2026, compared with its previous guidance of $4.5bn to $7bn. Its underlying EBIT forecast has also shifted from a previous range of minus $1.5bn to plus $1bn, to a clearly positive range of $2bn to $4bn.

Free cash flow expectations have also improved. Maersk now expects free cash flow of at least minus $1.5bn, compared with at least minus $3bn previously.

At the same time, Maersk has raised its outlook for global container market volume growth in 2026 to about 4%, compared with the previous range of 2% to 4%.

In other words, Maersk is not only expecting better freight rates. It is also taking a more confident view on global container demand.

A sharp change from the first quarter

The revision is notable because Maersk’s first-quarter results did not yet tell a strong profit story for its Ocean business.

In the first quarter of 2026, Maersk’s Ocean segment reported loaded volume growth of 9.3% and asset utilisation of 96%. However, average loaded freight rates were still under pressure, and the Ocean business posted an EBIT loss of $192m.

That was the second consecutive quarter of operating losses for Maersk’s core ocean shipping business.

At group level, Maersk remained profitable, supported by its Terminals and Logistics & Services divisions. But the message at that time was relatively cautious: volumes were strong, but freight rates remained weak and industry overcapacity continued to weigh on earnings.

Less than two months later, the picture has changed.

According to Maersk, the upgrade is driven by continued strong demand in the container market, particularly in the Far East, together with a recent sustained increase in spot market rates.

This is not a small adjustment. The lower end of Maersk’s EBITDA guidance has been raised by $3.5bn, while the upper end has been raised by $3bn. The EBIT outlook has moved from a range that still included a full-year loss to a range that points to clear profitability.

The implication is straightforward: container shipping earnings remain highly sensitive to freight rates. Once demand proves stronger than expected and spot rates rise, the profit outlook for liner operators can change very quickly.

China’s exports are supporting Far East cargo flows

Maersk specifically referred to strong demand in the Far East. Recent Chinese trade data helps explain why.

In the first five months of 2026, China’s total goods trade reached RMB 20.68trn, up 15.3% year on year. Exports rose 11.8% to RMB 11.91trn, while imports increased 20.5% to RMB 8.77trn.

In May alone, China’s total goods trade reached RMB 4.45trn, with monthly trade value exceeding RMB 4trn for the third consecutive month.

For the container market, this is an important background. It suggests that Far East export cargo volumes have continued to find support into the second quarter.

The structure of China’s exports is also relevant.

In the first five months, China’s exports of mechanical and electrical products reached RMB 7.58trn, up 18.4%, accounting for 63.6% of total exports. Exports of automobiles, electrical equipment and ships rose by 45.5%, 24.7% and 22.5%, respectively.

This means that Far East cargo demand is not being driven only by traditional consumer goods. It is also being supported by higher-value industrial, automotive, electrical, electronic and advanced manufacturing products.

These cargoes tend to place greater value on schedule reliability, space availability and network stability. When the spot market tightens, this can translate directly into stronger freight rates.

China’s trade partners also show a more diversified pattern. In the first five months, China’s trade with ASEAN, the European Union and Africa increased by 16.6%, 10.3% and 18.2%, respectively. Trade with Belt and Road partner countries rose 13.6%.

This suggests that China’s export resilience is not dependent on a single market. Far East cargo flows are being supported by Transpacific demand, intra-Asia trade, Europe, Africa and emerging market routes.

AI-related demand is adding another layer

Another factor behind stronger cargo flows is the rapid expansion of AI-related demand.

China’s official manufacturing PMI rose to 50.3 in June from 50.0 in May, returning to expansion territory. The new export orders index also improved from 48.6 in May to 50.1 in June, moving back above the 50-point threshold.

For liner shipping, this matters because the global AI investment cycle is increasingly being translated into physical cargo flows: chips, computers, servers, electronic components, data centre equipment and related hardware.

The current export strength is therefore not evenly spread across all product categories. It appears more concentrated in technology-related and advanced manufacturing supply chains.

This helps explain why liner companies are seeing stronger Far East demand. The cargo base is not only made up of low-value consumer goods or inventory restocking. It increasingly includes AI hardware, electronics, machinery, energy transition equipment and higher-value manufactured products.

Global trade has not collapsed, but supply chains remain disrupted

Global trade is showing signs of slowing, but it has not collapsed.

The WTO’s latest goods trade barometer showed the index easing from 102.3 in January to 101.7, suggesting some moderation in trade growth. However, the reading remains above the 100 baseline, indicating that global goods trade is still above trend.

This matches the current feel of the container market. Demand is not booming everywhere, but it remains resilient enough to matter.

At the same time, supply chains remain heavily disrupted.

The Red Sea crisis, tensions around the Strait of Hormuz, port congestion, rerouting, geopolitical risk and longer sailing distances have all continued to affect the efficiency of global liner networks.

For liner operators, these disruptions increase costs. But they also absorb effective capacity by lengthening voyages and reducing vessel turnaround efficiency.

That is the special feature of the 2026 container market.

On paper, the global container fleet is still facing heavy newbuilding deliveries and nominal capacity growth. In practice, geopolitical disruption, diversions, port delays and network restructuring are reducing effective capacity.

When demand remains resilient and effective capacity is being absorbed, spot rates become easier to support.

The rougher the seas, the more valuable reliable capacity becomes.

Freight rate sensitivity is back in the earnings model

Container shipping analyst Lars Jensen has also highlighted the scale of Maersk’s revision.

Based on Maersk’s first-quarter sensitivity guidance, a change of $100 per FFE in freight rates can affect full-year EBIT by around $1bn. A change of 100,000 FFE in volume has a much smaller impact.

On that basis, Jensen estimated that Maersk’s revised EBIT guidance may imply that the company now expects average full-year freight rates to be around $300 to $350 per FFE higher than it expected less than two months ago.

Because Maersk already knew its first-quarter rate levels when it issued its previous guidance in May, the upgrade is likely to reflect stronger expectations for the second, third and fourth quarters. On that basis, the implied rate improvement for the remaining three quarters could be even higher.

This is not an official Maersk number, but it provides a useful way to understand the revision.

The upgrade is probably not just about slightly higher cargo volumes. It is mainly about a much more favourable rate environment for the rest of the year.

Not every carrier will benefit equally

Maersk’s stronger outlook does not mean that all liner operators will benefit to the same extent.

First-quarter results already showed clear divergence across the industry.

According to Alphaliner’s comparison of major liner companies, the average core EBIT margin among leading container carriers was 5.2% in the first quarter of 2026. The industry as a whole remained profitable, but the gap between companies widened significantly.

Wan Hai, COSCO Shipping, Evergreen and HMM remained among the stronger performers, supported by Asian regional cargo flows, Far East exports and relatively lower exposure to weak Transatlantic markets.

By contrast, Maersk’s Ocean business, Hapag-Lloyd’s liner shipping segment and ZIM were already in operating loss territory in the first quarter.

This shows that earnings are not determined by freight rates alone.

Route structure, regional exposure, cargo mix, fleet cost, contract coverage, spot market participation, terminals, inland logistics and overall network flexibility all matter.

Maersk’s guidance upgrade shows that the market environment has improved materially compared with early May. But which carriers convert this rate rebound into real profit will depend on where they are exposed.

Carriers with higher exposure to Far East exports, stronger participation in spot markets and more flexible network deployment may benefit more directly.

Companies with heavier exposure to the Transatlantic, European exports or Middle East disruption may still face more complicated earnings pressure.

Second-quarter results will be the key test

Maersk is expected to report its second-quarter 2026 results in August.

The market will be watching three issues closely.

First, how much of the spot rate increase has already entered Maersk’s profit and loss statement.

Second, whether Far East export demand can remain strong through the second half.

Third, whether disruption in the Red Sea, the Strait of Hormuz and the wider Middle East will continue to support freight rates, or whether it will mainly add cost and operational uncertainty.

For now, Maersk’s revised guidance sends a clear signal: the 2026 container market has not weakened as quickly as many expected earlier in the year.

Instead, resilient demand, stronger Far East exports, higher spot rates and persistent supply chain disruption have pushed liner earnings expectations sharply higher.

This does not mean the industry has returned to the extraordinary profit cycle of the pandemic years.

But it does mean that the 2026 container market now looks much more profitable than it did when first-quarter results were released.

For liner operators, the next stage of competition will not simply be about who has the largest fleet. It will be about who can adjust networks faster, control key nodes, manage effective capacity and convert market volatility into earnings and cash flow.

READ MORE

Containers

Containers

How Can Sea Legend Reach Europe in 20 Days? Inside the Operational System Behind the CAX Arctic Express

Containers

Containers

Europe Is Sweltering at 40°C — Chinese Manufacturers and Shipping Networks Are Delivering the Cool

Containers

Containers

In 3 Days,Both Maersk and CMA CGM Bunker 100% Ethanol on Large Deep-Sea Containerships

Containers

Containers

Ningbo Containerized Freight Index Weekly Commentary Middle East Freight Rates Returned to High Levels; Composite Index Decline Narrowed

Containers

Containers

Maersk Partners With FAW Jiefang to Strengthen Global Supply Chain for Chinese Trucks

Containers

Containers

20 Days From China to Europe: Sea Legend Relaunches CAX Arctic Express with Eight Weekly Sailings

Containers

Containers

CMA CGM’s 13,000-TEU Giant Starts “Drinking” Too

Containers

Containers

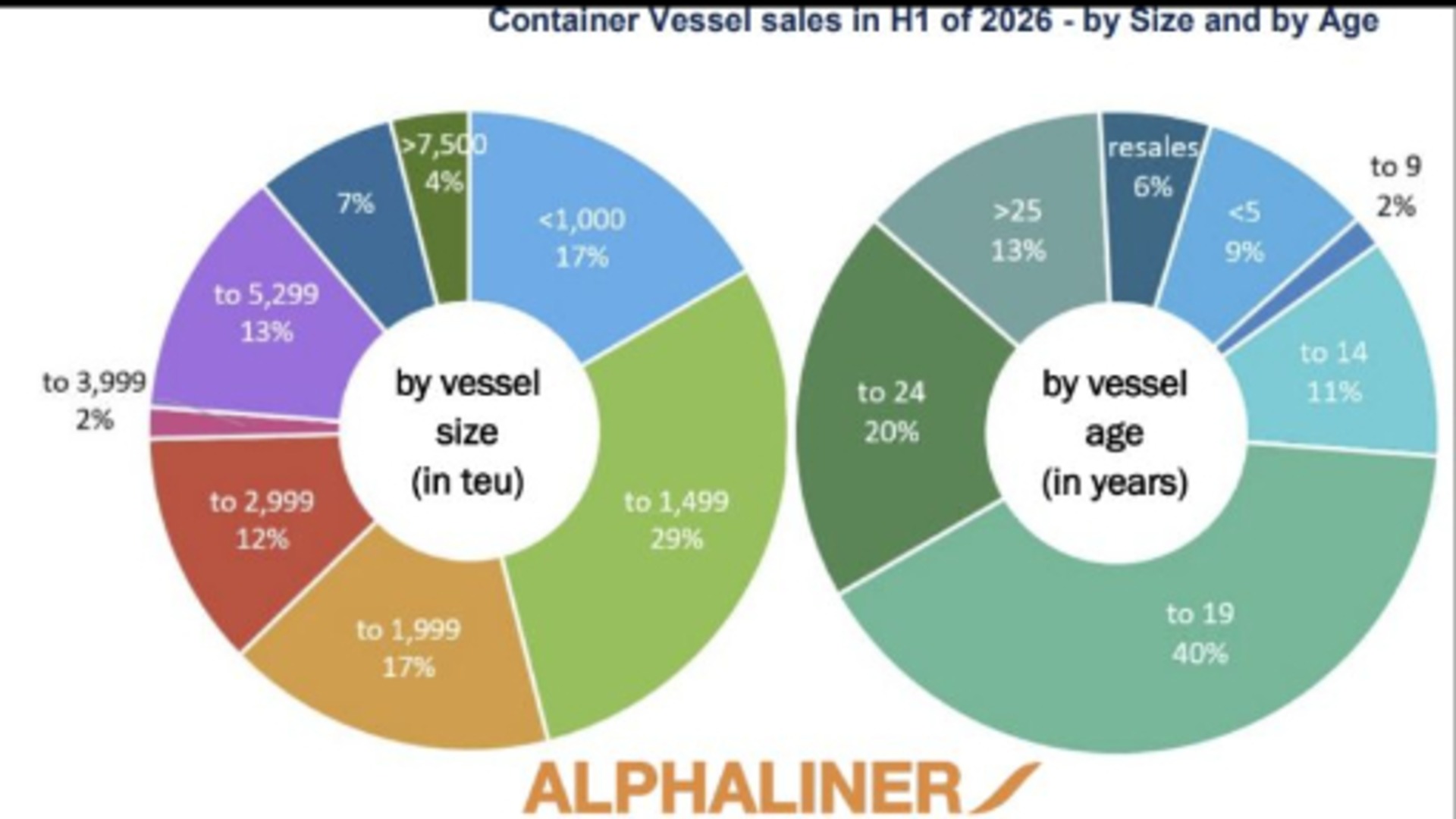

Secondhand containership sales fell sharply in the first half of 2026 — but vessel prices remained firm.

Containers

Containers

Ningbo Containerized Freight Index Weekly Commentary Overall Shipping Demand Declined; Freight Rates Fell on Multiple Routes

Containers

Containers