Nearly 400 VLCCs Have Been “Controlled”

A structural shift is taking place in the VLCC market, and it may be more important than today’s exceptionally high freight rates.

On paper, the global VLCC fleet remains large. But the key question for charterers, traders and investors is no longer simply how many VLCCs exist. The more important question is how many of them are still available as conventional, compliant, freely tradable tonnage in the mainstream charter market.

According to @Maritime Strategies International’s latest oil tanker market analysis, as of the first quarter of 2026, just under 40% of the global VLCC fleet fell into one of two categories: shadow/sanctioned tonnage, or VLCCs controlled by South Korea’s Sinokor.

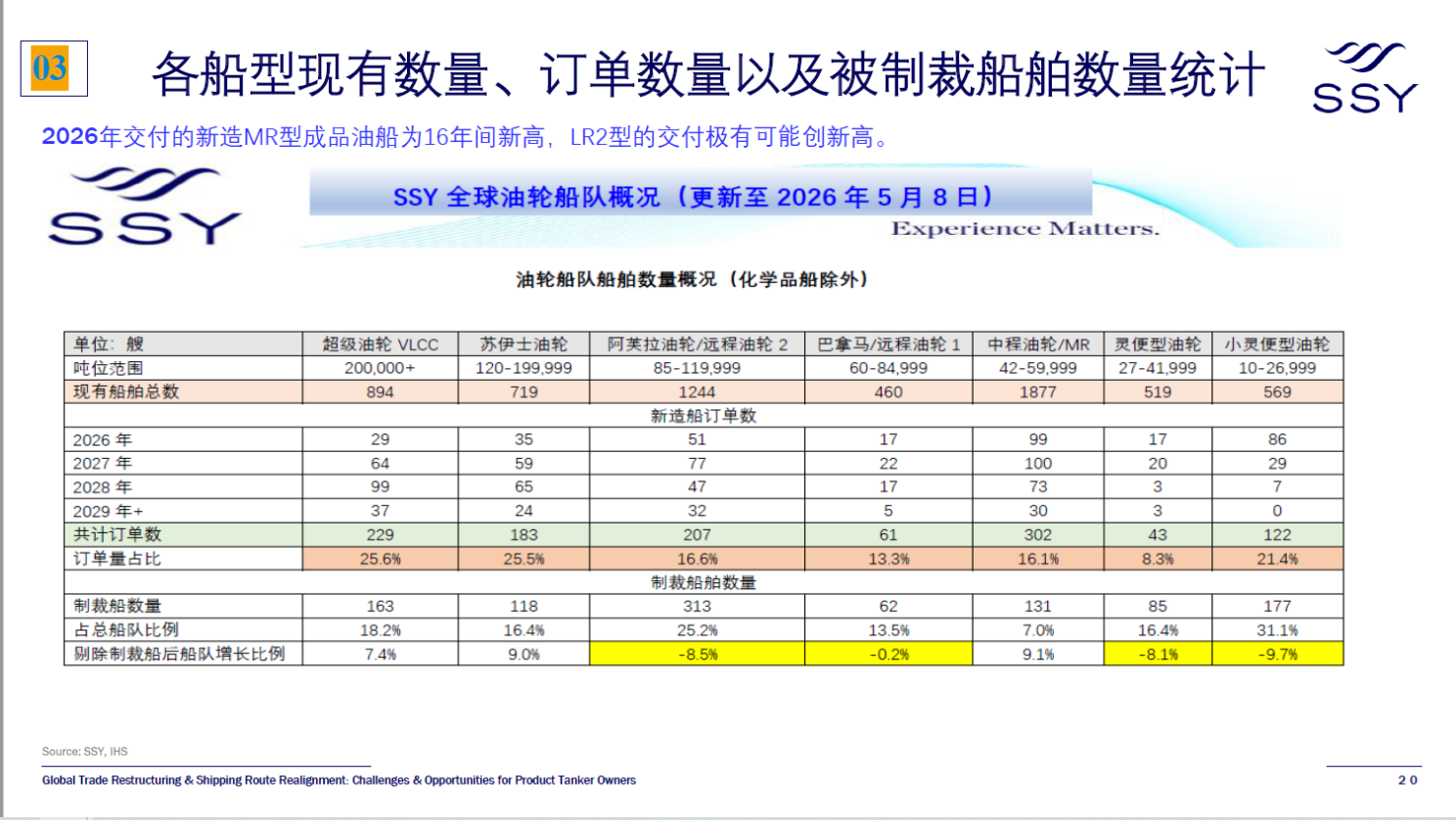

SSY data provided to Xinde Marine News shows the global VLCC fleet at around 894 vessels. On that basis, the number of VLCCs falling into these two categories is already close to 360 vessels — approaching 400 units in round terms.

That does not mean all these ships have disappeared from trading. It does mean a very large part of the global VLCC fleet can no longer be treated in the same way as ordinary open-market supply.

For a ship type that depends heavily on transparent chartering, mainstream oil company acceptance, bank financing, insurance cover and port access, this is enough to change the logic of market pricing.

A market being squeezed from two sides

MSI describes the VLCC segment as being increasingly squeezed by two forces: the expansion of the shadow fleet and Sinokor’s aggressive control of a large part of the VLCC fleet.

These two forces are very different in nature.

The shadow and sanctioned fleet is mainly linked to high-risk or sanctioned oil trades, including Russia, Iran and Venezuela. These vessels still form part of the global VLCC fleet on paper, but in operational terms many of them sit outside the conventional tanker market. They may trade through complex ownership structures, non-traditional insurance arrangements, opaque commercial chains and, in some cases, lower levels of operational transparency.

Sinokor-controlled tonnage is a different story. These ships are not necessarily sanctioned. Many remain compliant vessels. But when a large volume of VLCC capacity is concentrated under one platform, open-market liquidity is reduced. Sinokor has been one of the most aggressive players in the VLCC sale-and-purchase and chartering markets, rapidly expanding its influence through acquisitions, long-term control and related commercial arrangements.

The market implications become even more significant when MSC is added to the picture.

Reuters has reported that MSC is set to acquire a 50% stake in Sinokor through SAS Shipping Agencies Services, with MSC and the existing shareholder expected to jointly control the company if the transaction is completed. That would bring the world’s largest container shipping group directly into one of the most important VLCC platforms in the market.

For charterers, these ships have not vanished. But they are no longer equivalent to the old, fragmented, freely available VLCC pool that could be easily accessed by the wider market.

High earnings in a weaker demand environment

This helps explain one of the most striking contradictions in today’s VLCC market.

Crude flows from the Middle East have been heavily disrupted by geopolitical tensions and the restrictions around the Strait of Hormuz. Yet VLCC earnings have remained extremely strong.

MSI’s VLCC spot earnings benchmark averaged around $277,000 per day in April 2026. At the same time, traditional Middle East Gulf pricing benchmarks have become heavily distorted. The Baltic Exchange TD3C Middle East Gulf-China route was quoted at around WS400 at the end of May, while the newly released TD34 Gulf of Oman-China route was closer to WS130.

That gap shows how far traditional route benchmarks have moved away from real operational conditions.

On the demand side, Middle East crude loadings have fallen sharply. MSI estimates that Middle East crude loadings dropped by around 11 million barrels per day from January and February levels, to approximately 9 million barrels per day in April. Alternative export routes through Fujairah and, more importantly, Yanbu have helped offset part of the decline, but they cannot fully replace normal Middle East Gulf exports.

In other words, today’s high VLCC earnings are not simply a story of strong oil demand.

They are being driven by risk premiums, route dislocation, reduced effective supply and stronger control over available tonnage. When a charterer needs a compliant VLCC that is acceptable to mainstream cargo interests, insurers, banks and ports, the real choice is much smaller than the headline fleet number suggests.

This is the rise of “effective supply” pricing.

The shadow fleet is changing the base of the market

Over the past few years, the shadow fleet has moved from being a marginal issue to a central factor in tanker market analysis.

Sanctioned oil flows require ships. A large number of older VLCCs have therefore been drawn into special trading systems. These vessels continue to transport crude oil, but the boundary between them and the mainstream tanker market has become much clearer.

One layer of the VLCC fleet remains compliant, transparent, financeable, insurable and acceptable to mainstream charterers.

Another layer serves higher-risk trades, often with lower transparency and more limited access to the conventional market.

This segmentation has a direct impact on supply. The global fleet may look sufficient in headline terms, but part of that fleet is no longer available to many mainstream charterers under normal commercial conditions.

That becomes especially important when geopolitical risk increases, insurers tighten their appetite, banks strengthen sanctions screening, and ports become more cautious about vessel history and ownership structure.

As a result, future VLCC freight volatility will depend on more than OPEC production, Chinese crude imports and tonne-mile demand. It will also depend on sanctions enforcement, insurance availability, flag and class risk, AIS transparency, banking channels and charterers’ compliance policies.

The VLCC market is moving from a traditional supply-demand cycle into a market priced by compliance, geopolitics and control of tonnage.

Sinokor’s influence is about more than buying ships

Sinokor’s impact on the VLCC market should not be viewed simply as a buying spree.

In the secondhand market, Sinokor’s rapid acquisitions have absorbed a large amount of tradable VLCC tonnage, supported asset values and strengthened sellers’ expectations. For other buyers, similar vessels have become more expensive and harder to secure.

In the spot market, concentrated control over a large number of ships reduces the amount of capacity that can be immediately accessed by the open market. Even if these ships remain commercially active, once they are tied to a specific platform, customer base or long-term strategy, market liquidity changes.

From a capital perspective, the potential MSC-Sinokor link is even more important. If completed, the transaction would bring VLCCs into a broader global shipping capital allocation framework.

MSC has already reshaped container shipping through large-scale newbuilding orders, secondhand acquisitions and network expansion. If it enters the VLCC market through Sinokor, the tanker sector would face a very unusual new participant: a group with a vast global shipping network, strong capital resources and a clear record of long-term asset accumulation.

The impact on VLCC supply could still be at an early stage.

Newbuilding orders are rising, but they do not solve today’s problem

High freight rates and strong asset prices have also triggered a surge in VLCC newbuilding activity.

According to MSI, 90 VLCCs totaling 27.5 million dwt were ordered in the first four months of 2026, already exceeding the full-year contracting volume recorded in 2025. Five-year-old VLCC values are now above $140 million.

This shows that shipowners and capital providers are willing to pay very high prices to secure future VLCC exposure.

But newbuilding orders solve a medium- and long-term supply issue. They do not solve today’s effective supply shortage.

Most of these vessels will not enter the market until around 2028 or later. Today’s charterers are dealing with immediate issues: fewer freely available compliant ships, higher route risk, higher insurance costs and stricter compliance screening.

In the short term, as long as the shadow fleet continues to absorb part of the VLCC fleet, Sinokor-controlled tonnage continues to reduce open-market liquidity, and geopolitical risks continue to disrupt key loading regions, VLCC spot markets are likely to remain volatile and risk-premium driven.

In the medium term, newbuilding deliveries will test the market again. If Strait of Hormuz risks ease, special trading systems adjust, and refinery and crude trade patterns change, some of today’s high-priced newbuilding decisions may face a very different market after 2028.

That is the central tension in the VLCC market today: ships feel scarce in the short term, while the orderbook is building quickly for the future.

The next market question: how much of the fleet is truly usable?

There are now three key lines to watch in the VLCC market.

The first is the Strait of Hormuz. Whether transit normalizes, war risk costs decline, and mainstream oil companies and traders return to large-scale Middle East Gulf loading will directly affect how quickly VLCC earnings retreat from current highs.

The second is the shadow and sanctioned fleet. As long as high-risk oil flows linked to Russia, Iran and Venezuela continue to absorb VLCC capacity, the global market will remain segmented. A larger headline fleet does not necessarily mean more usable ships for mainstream charterers.

The third is the actual deployment strategy of Sinokor and MSC-linked tonnage. If these vessels are locked into long-term arrangements, internal systems or specific customer chains, open-market liquidity will remain tight. If some of them return more actively to the spot market, the pressure on rates could increase.

The core question for the VLCC market has therefore changed. It is no longer only about how many VLCCs exist globally. It is about how many VLCCs can actually be used by the mainstream market.

For charterers, the global fleet number is not enough. What matters is how many ships can be used under their compliance, insurance, port and contractual requirements.

For shipowners, owning a VLCC is no longer just about owning carrying capacity. It is about owning an asset that can remain acceptable to the mainstream market.

For investors, today’s VLCC earnings reflect both geopolitical risk premiums and a deeper revaluation of effective supply.

Nearly 40% of the VLCC fleet has already been reclassified by the combined forces of shadow/sanctioned trading and Sinokor control. That does not mean ordinary supply has collapsed, but it is enough to show that VLCCs can no longer be modelled simply by total fleet size.

The market that matters now is the compliant, transparent and freely deployable VLCC fleet.

READ MORE

Tankers

Tankers

16 Ships, RMB 778m in Profit: How Shanghai Beihai Shipping Broke Into China’s Top 20

Tankers

Tankers

Rubico Takes Over GSI-Built MR Tanker Contract from Top Ships in $45.2m Deal

Tankers

Tankers

Hormuz Chokes Again — and the VLCC Market Must Reprice Risk

Tankers

Tankers

Chinese Chemical Tanker Owner Dingheng Secures Million-Tonne Contract with PETRONAS

Tankers

Tankers

Shenghang plants flag in Singapore as Chinese chemical tanker owner goes global

Tankers

Tankers

Exclusive Interview | Trafigura’s Andrea Olivi: Ships and Ports Are Becoming Strategic Assets

Tankers

Tankers

Fratelli Cosulich Takes Delivery of Second Methanol-Ready Bunker Tanker

Tankers

Tankers

20-Year-Old VLCC Fetches $50M – Market Logic Turned Upside Down

Tankers

Tankers

First Ammonia-Fuelled Ship Loads Green Ammonia in China

Tankers

Tankers