European Route Freight Rates Enter a "Stepped Consolidation Phase"; Mid-July Rate Increase Window Remains Open

The European route has not entered a distinct downward channel. Mainstream shipping companies are utilizing the quote disparities between late June and early July to restructure their pricing systems, leaving room to maneuver for a new round of GRI (General Rate Increase) in mid-July. The core question for the current European route market is no longer "Can it rise further?" but rather "Can the previous gains be sustained?"

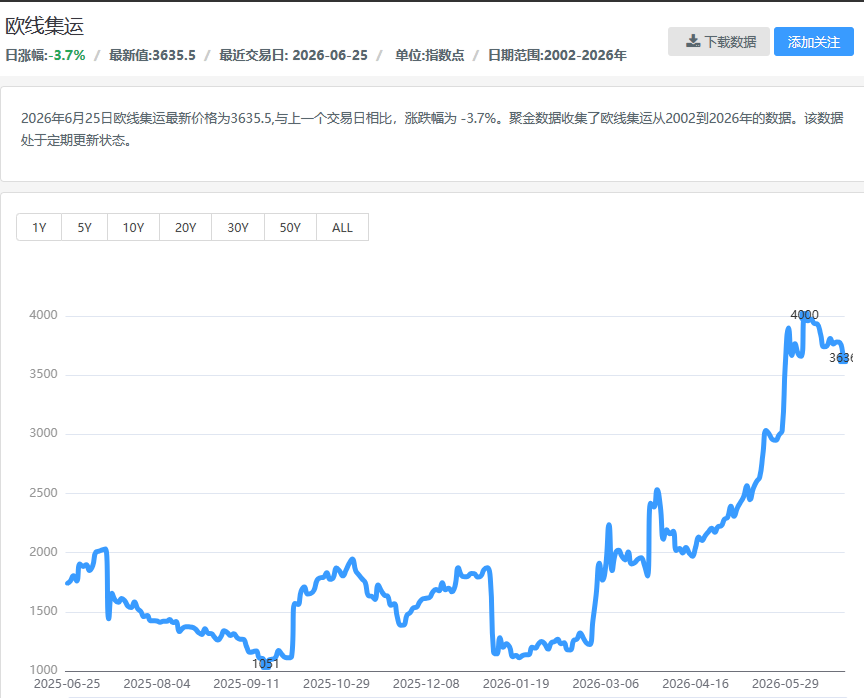

Freight rates on the European route are shifting from a "rapid surge" to "high-level consolidation" following consecutive increases.

This phase is highly susceptible to misinterpretation. When the market sees some quotes softening, it is easy to assume the price hikes have ended; when extra loaders (additional temporary vessels) appear, it is equally easy to assume supply-side suppression has begun. However, judging from the current quoting behavior of shipowners, the European route has not entered a clear downward trajectory.

On the contrary, mainstream carriers are leveraging the pricing gap between late June and early July to reorganize their pricing frameworks, paving the way for a new GRI—a collective or semi-collective move by carriers to elevate the market's price baseline—in mid-July. As long as the new price floor holds, there remains a possibility for further upward pushes in late July.

Top-Tier Carriers Raise Prices First, Market Realigns

The rhythm of this current round of rate increases is not characterized by synchronized action across all carriers. Instead, top-tier shipowners take the lead in raising the pricing anchor.

The significance of this move is not merely an extra $200 increase; it shifts the baseline for market negotiations up a notch. Under these circumstances, even if other shipowners do not fully match the hike, it becomes very difficult for them to maintain significantly lower prices. Once top-tier quotes are raised, the psychological expectations of freight forwarders and direct clients regarding the "market rate" are recalibrated. Subsequent adjustments by other carriers are more about finding an equilibrium for transactions within the new price range, rather than reverting to previous lows.

Therefore, the partial pullbacks seen in the market today should not be simply interpreted as carriers conceding on price. It is more akin to a structural correction following an initial price surge. The price gap between different carriers needs to narrow, and the rate differences between various destination ports must be realigned. The European route is not losing its support; it is reconfirming a new pricing center.

Extra Loaders Cause Disturbances, But Lack Real Suppressive Power

The market has been sensitive to extra loaders recently. While this variable warrants attention, one must look beyond simply "whether there are extra loaders" and assess whether they form a continuous, stable, and large-scale supply of effective capacity.

Currently, the impact of extra loaders on the European route remains limited. The rollout of some temporary voyages has not been smooth, with uncertainties surrounding sailing schedules, port calls, container sourcing, and destination port connections. The small extra loaders recently added by Hapag-Lloyd act more as localized supplements rather than new capacity capable of reshaping the supply-demand dynamics of the route.

More importantly, in a high-freight-rate environment, extra loaders will not necessarily initiate price cuts. As long as there is cargo available and space can be sold at a premium, temporary voyages are more likely to follow high market prices rather than destroy the mainstream carriers' pricing system with low rates.

The true threat to freight rates is not sporadic extra loaders, but rather the continuous release of large-scale extra capacity undercutting the market to grab cargo. The market has yet to witness this type of supply shock. The so-called pressure from extra loaders is currently more of a psychological disturbance than a decisive variable dictating price trends.

Groundwork for the Mid-July GRI Has Begun

The next critical window for the European route remains mid-July.

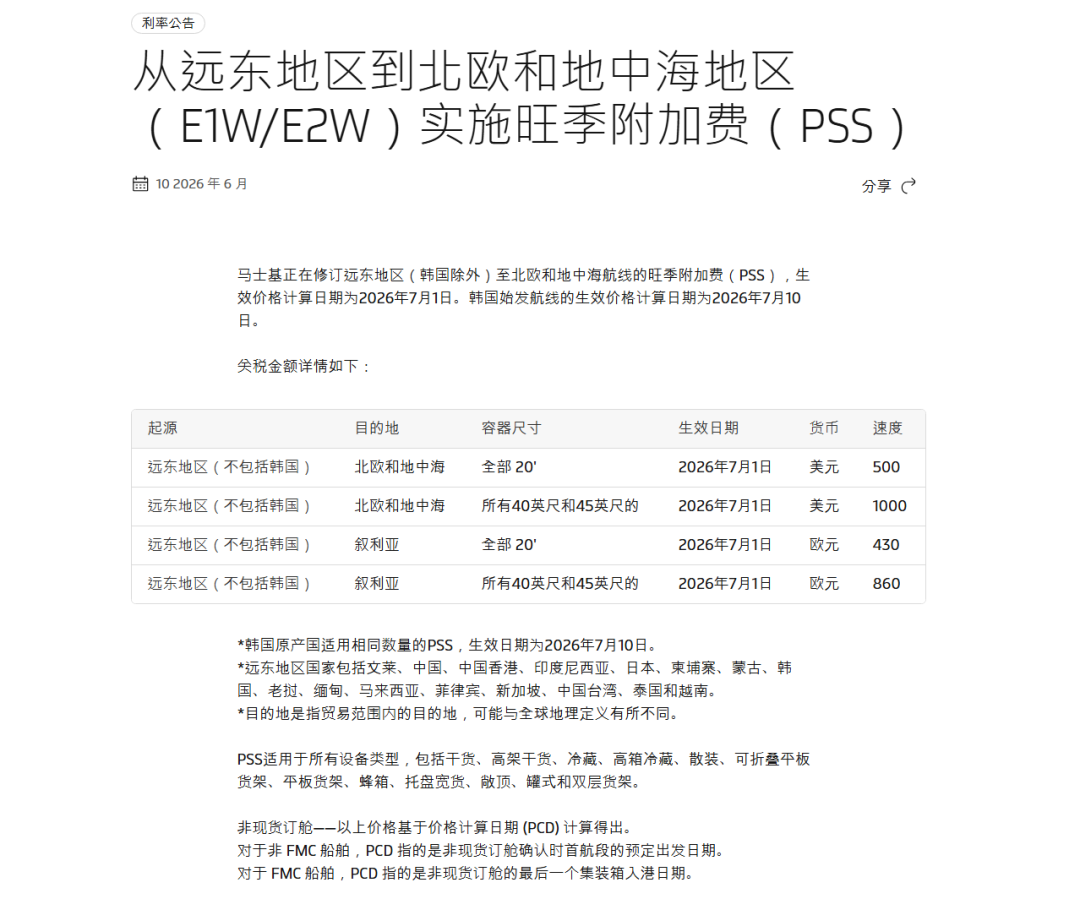

It is highly probable that several foreign carriers will continue to drive this round of GRI. This assessment is based not on verbal statements, but on the fact that they have already begun adjusting their pricing structures. Maersk's continued upward adjustment of quotes for WK28 (Week 28) indicates that top-tier carriers are in no rush to release cheap capacity. Carriers like MSC and Hapag-Lloyd have also proactively raised the price bracket for early to mid-July through FAK (Freight All Kinds) rates, PSS (Peak Season Surcharges), or varied route quotes.

What shipowners are doing right now is stabilizing the price floor for early July, positioning mid-July as the next price reset window. If the load factor does not significantly weaken during this period, the GRI around July 15 will have a strong foundation for execution.

Naturally, whether the GRI can be fully realized depends on cargo volumes and capacity. But for shipowners, even a partial realization is enough to maintain a high-level market. As long as the market doesn't rapidly plummet below the current price band, carriers will continue attempting to push transaction levels higher in late July.

Not a Trend Reversal, But a High-Level Gear Shift

The current divergence in European route prices is essentially a "high-level gear shift."

In the preceding phase, carriers needed rapid price increases to repair depressed freight rates. Quotes during that phase were aggressive, with high price elasticity. In this current phase, carriers are more focused on stabilizing market expectations and translating previous gains into actual transaction prices. This phase naturally brings quote corrections, narrowing price gaps, and a wait-and-see approach from clients.

Therefore, short-term quote softening does not mean the freight rate cycle is over. The true indicators to watch are:

Do top-tier carriers maintain high quotes? If mainstream carriers like Maersk do not obviously abandon their high prices, the market floor will not easily collapse.

Do extra loaders transition from sporadic disturbances to continuous supply? If they remain small-scale gap-fillers, their impact on mainstream prices will be limited.

Can early July load factors support the mid-July GRI? If carrier capacity continues to sell smoothly, the rate increase window will not easily close.

Current conditions indicate that these three variables do not point to a definitive downward phase for the European route. A more accurate assessment is that the market is transitioning from rapid, aggressive hikes into a transitional period of high-level consolidation and subsequent test hikes.

Market Outlook: Upward Momentum Remains for Late July

The subsequent trajectory of the European route will likely not be a unilateral surge, nor will it be an immediate, sharp decline. Instead, it will experience high-level fluctuations while awaiting a new round of price confirmation.

Scenario 1: Synchronized Execution of GRI If the July 15 GRI achieves synchronized execution by major carriers, European route freight rates will continue to test upward. Even if the rate increases are not fully realized, prices may still remain in a relatively high range. This is because top-tier carriers have already completed a round of price hikes, and the market's new negotiation baseline has changed.

Scenario 2: Slight Price Concessions by Some Carriers If some carriers make slight price concessions to secure load factors, the market will not necessarily weaken immediately. As long as these concessions still occur within a high price range, it is merely price consolidation, not a trend reversal.

⚠️ Two Situations to Watch Out For First, a sudden and concentrated increase in extra loaders releasing capacity at low prices; second, a significant weakening in July cargo volumes, leading to a concentrated exposure of carriers' load pressures. Until these two situations emerge, the European route maintains strong short-term support.

Overall, the prevailing theme for the European route is not "the end of rate increases," but rather "post-hike price reconstruction." Top-tier carriers have raised the pricing steps, and other carriers are recalibrating around this new range. The mid-July GRI will serve as the next validation point. Assuming the supply side does not lose control, European route freight rates still have the opportunity to test upward movement after this period of high-level consolidation.