Potential risks from the fallout of IMO 2020 are lying dormant as the industry stares down the immediate challenge of a sharp downturn in global seaborne trade.

A combination of weaker demand due to the coronavirus and warm winter, strategic buying of clean marine fuels ahead of the deadline and a greater supply of middle distillates from refiners has overshadowed concerns around fuel quality and availability. But rougher waters may lie ahead.

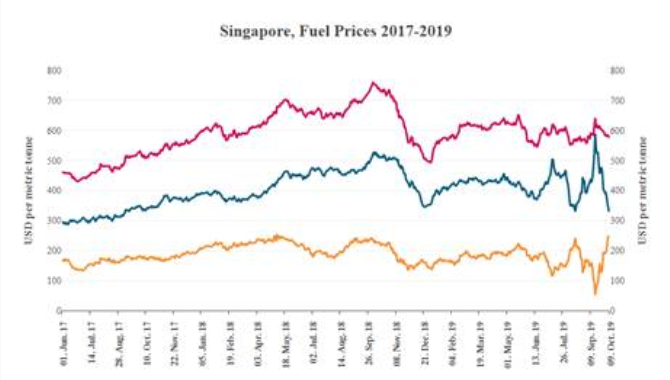

While the price of bunker fuel, especially VLSFO has fallen as a result of the demand weakness, refiners may need review plans to desulfurize their fuel oil pool to help rebalance product markets. That could drive prices much higher for VLSFO and middle distillates, while high sulfur fuel oil prices should continue to fall.

The executive vice president of Hungarian energy firm MOL Ferenc Horvath in an interview with S&P Global Platts Monday said he believes “the real impact of IMO” won’t be seen until “April or May”, given the uncertainty around the available data.

Quality issues

The biggest threat comes from quality issues of very low sulfur fuel oil, which will likely end up as the fuel of choice from the bulk of the industry. Sedimentation, stability and compatibility questions remain unresolved. The industry has debated the risks of sediments along with co-mingling paraffinic and aromatic balances in fuels leading to sludge clogging up engines – unlike in a car where all gasoline can be used regardless of the supplier.

“IMO is very real and will outlast coronavirus issues,” said S&P Global Platts Analytics’ Rick Joswick, global head of oil pricing and trade flow analytics. “The warm winter impact on distillate demand and coronavirus impact on jet demand are masking the IMO upside demand on MGO [marine gasoil] — but everything else associated with IMO is still fully in play,” he added.

BIMCO analyst Peter Sand believes the risk is something that the industry can handle. “The issue on sediments is no bomb – but obviously an issue for the refiners to deal with. The marine industry is used to burning residual fuel oil, sometimes containing ‘disrupting stuff’ too. But for bunker tanks, filters and engines this is an operational issue. Cumbersome to deal with but manageable,” he said. “Having said that, fuel supplied to the industry should not generate problems like that,” he added.

In general, the wealthiest and most organized shipowners will fare best with the new fuels. Those who are able to pay a premium for fuels with a global compatibility guarantee, and those able to plan their ships’ schedules weeks or months in advance and arrange the availability of the right fuels accordingly, will largely be able to avoid problems. Marine gasoil may be a premium product, but confidence has grown in VLSFO in a credit-hit shipping sector that prefers to get the cheapest fuel possible.

Conversely, shipowners seeking to minimize costs, ships on the spot market with little control over their ports of call will bear the brunt of the disruption caused as the industry experiments with the new bunkers.

Availability concerns

The key hubs such as Singapore, Fujairah and Rotterdam have all been well stocked in VLSFO, while shippers rushed to snap up cleaner fuels to avoid any panic. There was an initial rush to procure VLSFO due to availability concerns at the start of January. Since then demand for VLSFO has slowed, putting downward pressure on prices and widening the spread between it and MGO. When these stocks start to run down, or ships sail to and from smaller ports, compliance may return as a genuine question.

“Fuel availability in major hubs was not an issue, and we do not expect it to be an issue for ‘the second wave’, when all ships will refuel low sulfur bunkers in coming weeks and months,” Sand also said. “Naturally, we are worried that bunker supplier once again will take advantage of the situation commanding a massive premium, not based on any fundamental factors,” he added.

From March 1 carriage of marine fuel with more than 0.5% S in any of the ship’s tanks will mean the vessel is falling foul of regulations, even if they aren’t using it. Moreover, port states will have authority to enforce the rules, not just flag states.

“Anyone who had planned for a debunkering of HSFO in China to take place in February will need to find somewhere else to get the job done. Naturally an unpleasant disruption for those owners and operators,” Sand added.

Supply has also been ample as the oil industry geared up to produce as much middle distillates as possible. The price of VLSFO has come down after spiking earlier this year and late 2019, with refiners diverting vacuum gasoil from gasoline to VLSFO production to take advantage. Heavy sweet crude grades such as Australia’s Pyrenees, which are suited to generating cleaner marine fuels due to being distillate-rich and low in sulfur, have also come off their peaks after eyeing headline-inducing $100/b levels (trading at a $31/b premium over Dated Brent) earlier this year.

So keeping an eye on margins and several key price/demand battles define the months ahead, including between gasoline and the distillate-led middle of the barrel and also within the squeezed middle between marine gasoil and VLSFO.

Source:Platts

The opinions expressed herein are the author's and not necessarily those of The Xinde Marine News.

Please Contact Us at:

admin@xindemarine.com

.gif)

Baltic Exchange launches new Fuel Equivalence Conve

Baltic Exchange launches new Fuel Equivalence Conve  21 Consecutive Years of QUALSHIP 21 Recognition for

21 Consecutive Years of QUALSHIP 21 Recognition for  MPA and Wärtsilä Renew Partnership to Drive Marit

MPA and Wärtsilä Renew Partnership to Drive Marit  MPA and Dalian Maritime University Renew Partnershi

MPA and Dalian Maritime University Renew Partnershi  PSA INTERNATIONAL, DNV AND PACIFIC INTERNATIONAL LI

PSA INTERNATIONAL, DNV AND PACIFIC INTERNATIONAL LI  INTERCARGO Reaffirms Call for Simplicity as IMO Cli

INTERCARGO Reaffirms Call for Simplicity as IMO Cli