The green transition of the shipping industry is picking up pace with shipowners starting to invest in vessels that are technologically prepared to burn alternative fuels such as ammonia and hydrogen.

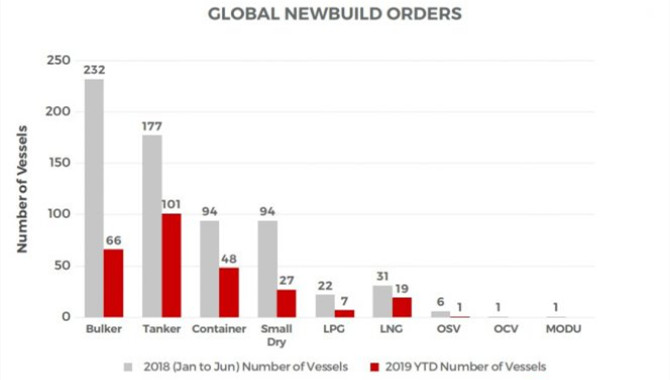

Uptake of alternative fuels has continued to progress, with 4.8% (2021: 3.7%, 2017: 2.3%) of the fleet on the water and 43.8% (2021: 28.2%, 2017: 10.4%) of the orderbook in tonnage (GT) terms capable of using alternative fuels or propulsion.

LNG and other alternative fuels make up 4.5% of the fleet when looking at the gross tonnage and 44% of the orderbook, data from Clarksons Research shows. This is a record share for alternative fuel orders in 2022, comprising 59% of all newbuild orders by tonnage.

For context, in 2021 31.5% of newbuild tonnage ordered was capable of running on alternative fuels (479 units), up from 211 orders in 2020 and 46 orders in 2016.

Of the orderbook, 38.9% of tonnage is set to use LNG (781 units), 2.2% to use LPG (86 units) and 4.3% due to use other alternative fuels (c.260 units; including methanol (42), ethane (11), biofuels (5), hydrogen (12) and battery/hybrid propulsion (c.200)).

With future optionality over fuel choice continuing to gain traction, there are now over 320 “LNG ready” ships in the fleet and 99 on the orderbook, while there are 130 “ammonia ready” and 6 “hydrogen ready” vessels on order.

These include vessels that have been deemed multiple fuels / fuel ready to provide future optionality.

Scrubbers are now fitted to over 4,838 ships in the fleet (including pending retrofit), equivalent to 24.9% of total GT. While scrubber retrofitting activity has slowed (September 2020: ~120 per month, September 2022: ~15 per month), newbuild uptake grew slightly in 2021, while 60 scrubber fitted units have been ordered in 2022 so far. The current price differential between HSFO and VLSFO remains highly significant (Rotterdam/Singapore: $210/$320), having reached record highs earlier in the year.

·Energy-saving technologies (ESTs) have been fitted on over 5,550 ships, accounting for 24.5% of fleet tonnage: this includes propeller ducts, rudder bulbs, Flettner rotors, wind kites, air lubrication systems and others.

·Carbon capture scrubber uptake is in “early days” and only 19 vessels have installations fitted / pending.

·BWMS retrofit programme ongoing: majority of fleet tonnage (70.6%) now BWMS-fitted.

·Ports globally with LNG bunkering have increased from ~60 to ~150 in past five years and may reach ~250 by 2026. Huge investment at ports is needed: only 171 ports (out of ~6,000) have shore side power, while over 1,700 vessels are fitted/set to be fitted with shore power connections;

“Although shipping’s huge fleet renewal program is in its infancy, we are already seeing “tiered” markets develop. By the end 2023, we project that 30% of the fleet tonnage will be modern “eco”, 24% will be scrubber fitted, 6% will be alternative fuelled and 25% will have an Energy Saving Technology (EST),” Clarksons said.

“Besides emissions, we expect a record fuel bill for shipping in 2022 to increase focus / premiums for fuel efficient tonnage. The scrubber retrofitting peak has passed (20 per month from 200 in 2020), recent price spreads have justified some scrubber investment and there has been an associated small pick up on newbuilds fitted with scrubbers.”

Even though the preparation of the global regulatory framework has been somewhat slow in spurring the acceleration of the sector’s decarbonization process, there are growing pressures to impose more ambitious targets and move beyond current IMO commitments towards 2050 “net zero” from 50% GHG reduction agreed today.

Furthermore, industry bodies are urging for a well-to-wake approach to calculating emissions of alternative fuels as a way of ensuring overall emissions reduction targets are achieved. As explained by Clarksons, this has created the likelihood of regional divergence and complexity (e.g. EU, US).

As eco ships start to take a growing share of the fleet (‘modern’ eco vessels now 28.9% of total GT), various implications for earning potential, asset values, and charter market complexity are emerging. Clarksons estimates that 26.6% of global tonnage was “eco” twelve months ago, and just 14.6% at start-2018.

Shipping Industry Emissions: 850mt & 2.3% of global CO2

Shipping contributes 2.3% of global CO2 emissions (2008: ~1bnt of CO2, 3% of global). After a Covid-19 related decline and then increase, as trade volumes rebounded, Clarksons is projecting emissions to remain steady next year as the impact of speed and a growing “eco” fleet balance any trade and fleet activity growth.

Although vital progress is still needed, shipping emissions have trended downwards since 2008 (down ~17%, achieved principally by a ~20% drop in speed and in part by fuel-efficient designs, while moving 40% more cargo and with 90% more tonnage involved) and shipping remains the most “carbon efficient” mode of transport (x3 rail and x11 truck).

That being said, the average age of the world fleet is increasing, standing at 12.2 years on a GT weighted basis (up from a low of 9.7 years in 2013). For the bulk carrier fleet, the average age is 11.5 years, for tankers it is 12.1 years and for the container fleet it is 14.2 years. Today, 28.1% of global tonnage is aged over 15 years.

The overall orderbook as a % of fleet capacity is ~10% – the figure is 27.2% for containers, 7.0% for bulkcarriers and 4.5% for tankers.

“We are now less than three months from the entry into force of IMO’s 2030 short-term measures involving segment-specific minimum ship-by-ship efficiency standards in 2023 (EEXI) and an annual efficiency improvement program (CII) based on operational performance thereafter (data for the CII will be collected across a year). Our theoretical CII rating estimates suggest around a third of vessels will be D or E rated if current operational behaviour continues (~29% for tanker, 33% bulker, 29% container), rising towards 50% if they are still trading in 2026 and have not modified speed or specification,” Clarksons said.

The prevailing propulsion technology uncertainty and associated residual value risk concerns are contributing to a relatively short orderbook (still ~10% of fleet) and expectations of relatively low fleet growth in the medium-term. As a result, it is unlikely that the unprecedented fleet renewal needed to decarbonise will progress evenly.

Clarksons estimates that emissions policies could impact supply / demand balances via changes in chartering policies, demolition levels and, in particular, speed with upside volatility for freight / charter rates. Namely, average container vessel speed is down 25% since 2008.

“Our scenarios suggest total newbuild orders will increase from $64bn (2016-2020) to $139bn a year (2021-2030). We project $1.4 trillion of newbuild orders needed for fleet renewal 2021-2030 and $4.2 trillion through 2050). Our scenarios illustrating approaches to decarbonisation involve a number of “levers” including speed (emissions, and overall vessel supply, are responsive to even small drops in speed), fuel type, the volume and geography of trade and transportation efficiency (also improved via digitalisation technology). All of these levers can significantly impact market supply / demand balances, with both upside and downside potential. Financing fleet renewal (+shoreside infrastructure), may become a long-term challenge without new sources or “green” credentials established,” the shipbroker said.

Source: Offshore Energy

The opinions expressed herein are the author's and not necessarily those of The Xinde Marine News.

Please Contact Us at:

media@xindemarine.com

.gif)

WOODSIDE AND CHINA RESOURCES AGREE LONG-TERM LNG SU

WOODSIDE AND CHINA RESOURCES AGREE LONG-TERM LNG SU  Shanghai Yangshan Port Bunkered Two LNG Powered Con

Shanghai Yangshan Port Bunkered Two LNG Powered Con  Headway successfully delivers filtration skid solut

Headway successfully delivers filtration skid solut  Celebrating the Launch of “Green Energy Pearl” –

Celebrating the Launch of “Green Energy Pearl” –  PIL and SSES complete the inaugural LNG bunkering o

PIL and SSES complete the inaugural LNG bunkering o  BW LNG secures e-procurement deal with Procureship

BW LNG secures e-procurement deal with Procureship