The spot price of iron ore is being pushed higher in a pincer move of stronger Chinese demand and lower supply from the world’s two biggest exporters of the steel raw material.

The spot price of benchmark 62% iron ore for delivery to north China, as assessed by commodity price reporting agency Argus, rose to $128.80 a tonne on Monday, just shy of the peak so far in 2023 of $129.50 reached on Jan. 30.

The price has gained 5.7% over the past week and is now 63% higher than the 2022 low of $79 a tonne, hit on Oct. 31.

The gains are being driven by restocking by steel mills in China, which buys about 70% of global seaborne iron ore and produces half of the world’s steel.

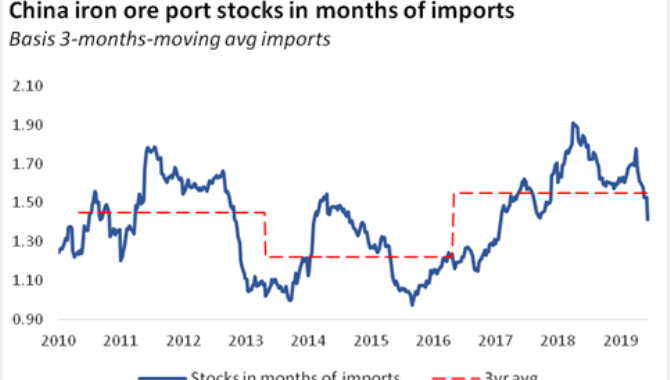

Iron ore inventories at Chinese ports rose to 140.9 million tonnes in the week to Feb. 17, up from 138.35 million the prior week, and up from the pre-winter low of 130.2 million from the week to Oct. 14.

It’s worth noting that stockpiles remain well below the same week last year, when they were at 160.95 million tonnes.

China’s iron ore inventories typically build over the winter period as construction activity winds down, but stockpiles then tend to draw down from March onwards as steel production ramps up to meet rising demand as building work accelerates.

With Beijing working to stimulate the economy after ending its strict zero-COVID policy that hindered growth last year, expectations are that infrastructure and construction activity will pick up from the second quarter onwards.

Easier monetary policy and loans are among measures aimed at boosting construction, and another pilot scheme to boost private investment in real estate was announced on Monday.

China’s iron ore imports appear set for a strong February, with commodity analysts Kpler estimating arrivals of 100.22 million tonnes, which at 3.58 million tonnes a day would exceed the 3.48 million that landed in January.

China’s steel prices are also rising on expectations of stronger demand, with benchmark Shanghai Futures Exchange rebar contracts SRBcv1 ending at 4.167 yuan ($608.32) a tonne on Monday, up 3.4% over the past week.

SUPPLY SLUMP

It’s not only the demand side that is working to boost iron ore prices, with some concerns over the state of supply from the world’s two biggest exporters, Australia and Brazil.

Australia’s iron ore exports are likely to drop in February, with Kpler estimating shipments of 57.7 million tonnes, while Refinitiv is forecasting 58.74 million.

While these figures are likely to be revised higher as more cargoes are assessed prior to month end, it’s likely that February’s exports will fall well short of Kpler’s figure for January shipments of 79.64 million and December’s 84.58 million.

Brazil’s exports are likely to recover somewhat in February after being hit by weather disruptions in January, with Kpler estimating shipments of 28.57 million tonnes and Refinitiv expecting 29.48 million.

This would be up from January’s exports of 22.91 million, which Kpler data showed were Brazil’s weakest since February last year.

While Australia and Brazil dominate the global seaborne iron ore trade, it’s worth noting that other exporters aren’t adding much to the overall supply story.

South Africa, the world’s third-largest exporter, is forecast to ship 4.12 million tonnes in February, down from January’s 4.59 million, while India is expected to export 1.48 million, down from 3.49 million.

The supply shortage and expectations of increasing Chinese demand are likely to provide a solid base for further gains in spot iron ore prices.

However, it’s likely that supply will return to normal levels in coming months, which may cap the upside potential.

The other factor is whether the market’s optimistic view on the likely success of China’s stimulus plays out in reality, or whether it takes longer than anticipated to fire up the world’s second-biggest economy.

Source: Reuters

The opinions expressed herein are the author's and not necessarily those of The Xinde Marine News.

Please Contact Us at:

media@xindemarine.com

.gif)

PIL launches Academy to strengthen workforce compet

PIL launches Academy to strengthen workforce compet  Coal shipments to advanced economies down 17% so fa

Coal shipments to advanced economies down 17% so fa  China futures market updates at close (Nov 14)

China futures market updates at close (Nov 14)  CISA: China's daily crude steel output down 5.7% in

CISA: China's daily crude steel output down 5.7% in  China futures market updates at close (Oct 31)

China futures market updates at close (Oct 31)  CISA: China's daily crude steel output down 1.2% in

CISA: China's daily crude steel output down 1.2% in