Disruptions to steel production in China due to lockdowns to curb Covid-19 outbreaks will offset the impact on steel prices from weak demand in 1Q22, and market dynamics should improve from 2H22, Fitch Ratings says.

We expect steel demand to improve from 2Q22 on investments in infrastructure and a bottoming out in the property market, while producers remain disciplined about supply.

Construction activities, the main driver of steel demand, were weak during the first two months of 2022, partly due to seasonality related to the Chinese New Year holidays, and were worsened by lockdowns across the country to curb the spread of Covid-19 and a weak property market. In contrast, fixed-asset investments in infrastructure and manufacturing grew by double digits, and we expect this to translate into strong growth in construction in 2Q.

Supply remained disrupted in 1Q22 due to the winter heating season and the Winter Olympics in Beijing, which were anticipated, as well as unexpected city-wide lockdowns. For example, Tangshan, the city responsible for almost 15% of the country’s total steel output, has been in lockdown since 20 March. The lockdown resulted in estimated daily production loss of 30,000-35,000 tonnes as of 24 March. Fitch estimates. The restrictions also delayed steel-product deliveries to customers and hampered deliveries of raw materials to steel plants, which could extend production losses if the lockdown continues.

As a result, we expect a limited impact on steel prices, despite weaker demand in March and April 2022, as the supply disruptions remain in place until the Covid-19 infections stabilise. We also expect demand to recover quite strongly in 2Q22 when the lockdowns are lifted.

In addition, Fitch expects the costs of raw materials, such as iron ore and coal, to remain high in 2022 due to geopolitical tensions and state-mandated measures to reduce carbon emissions.

Therefore, we expect steel prices to remain fairly high, with margin pressure coming from highercosts.

Companies that are more self-sufficient in terms of raw materials, such as Shougang Group Co., Ltd.(A-/Stable), China Baowu Steel Group Corporation Limited (A/Positive) and HBIS Group Co., Ltd.

(BBB+/Stable), are likely to outperform the industry. Steelmakers with higher value-added products that cater to sectors such as new infrastructure and auto, including HBIS and Baowu, will also fare better than those that produce conventional low value-added products or have low raw-material self-sufficiency such as Guangyang Antai Holdings Limited (B/Stable).

Source: Fitch Ratings

The opinions expressed herein are the author's and not necessarily those of The Xinde Marine News.

Please Contact Us at:

media@xindemarine.com

.gif)

PIL launches Academy to strengthen workforce compet

PIL launches Academy to strengthen workforce compet  Coal shipments to advanced economies down 17% so fa

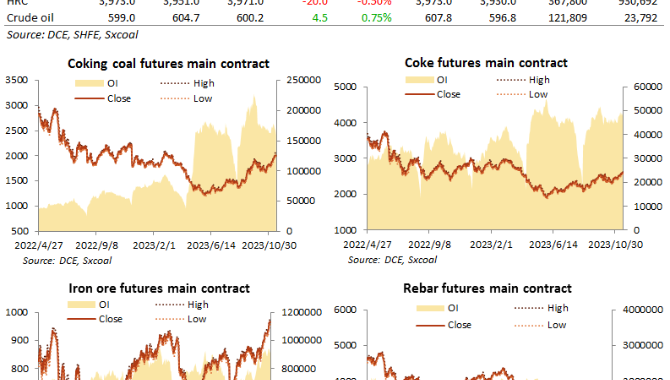

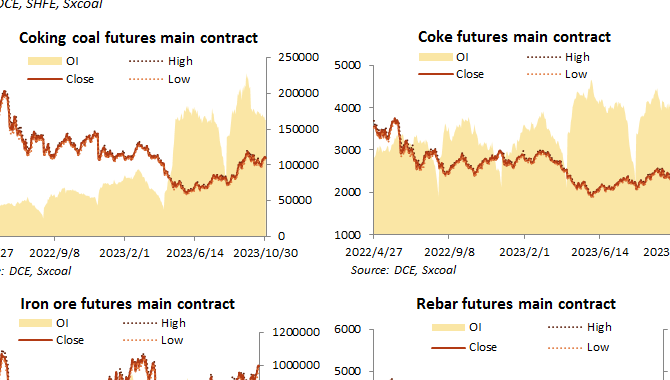

Coal shipments to advanced economies down 17% so fa  China futures market updates at close (Nov 14)

China futures market updates at close (Nov 14)  CISA: China's daily crude steel output down 5.7% in

CISA: China's daily crude steel output down 5.7% in  China futures market updates at close (Oct 31)

China futures market updates at close (Oct 31)  CISA: China's daily crude steel output down 1.2% in

CISA: China's daily crude steel output down 1.2% in