Over the past few challenging months, iron ore has been the standout commodity, returning to prices of $100/metric ton (delivered to China) in late May for the first time since August 2019.

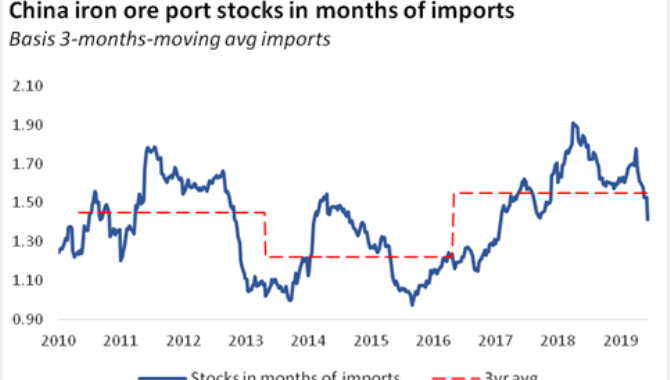

Demand for the key steelmaking raw material has been extremely resilient this year, supported by strong crude steel production in China, supply shortages and lower iron ore stocks at Chinese ports. China produced a record 92.27 million mt of crude steel in May, up 4.2% on the year, and June has kicked–off strongly, National Bureau of Statistics data shows.

Most analysts had predicted that benchmark 62% Fe iron ore prices would fall to around $70/mt CFR this year on the basis there was plenty of supply coming from Australia and Brazil. Demand from Chinese steelmakers was expected to pick up as economic activity resumed after coronavirus-related lockdowns, even though steel production growth appeared to be outpacing demand growth and steel inventories were more than double usual levels. Some participants thought this would result in a slowdown of steel production. But so far this hasn’t happened.

Instead, the second half of this year looks set to be a bumper one, due to pent-up demand and government efforts to support infrastructure and property. Beijing has modest expectations for the economy this year, hence its decision not to provide a GDP target. But the government needs to keep the economy robust in the face of weak export markets, a potential ramping up of tensions with the US, and most importantly to ensure job losses are not too severe.

Compared to steel companies around the world, Chinese steel mills are doing well because downstream activity has largely recovered, whereas other countries are still in various stages of lockdown. On June 12, steelmaker margins (the price of finished steel after subtracting input and other costs) in China for domestic rebar used in construction was $72/mt. The margin for hot-rolled coil, which is the main steel product used in manufacturing, was $35/mt on that day, according to S&P Global Platts analysis of finished steel and raw materials prices.

China has found itself the target for steel exports from India, South Korea, Turkey and Russia because the steel prices on offer are higher than in other markets. Normally, these arbitrage opportunities do not last long. But outside of China, steel companies are still trying to gauge their production to match the pace of economic recovery. Some Indian steel companies are trying to lift their steel output but are having to export up to 70% of their production because India is only slowly coming out of lockdown.

In Europe and the US, steel production levels have been substantially lowered because the coronavirus outbreak is still severe in places. Manufacturing and car production have been hit extremely hard. Most people in the market do not expect any decent recovery until the final quarter of this year. This means there will be plenty of pressure on prices in Q3.

China’s steel market is largely inured to the worst of the global steel downturn and can survive and prosper on domestic steel demand alone. This is likely to support iron ore prices while shortages from Brazil persist.

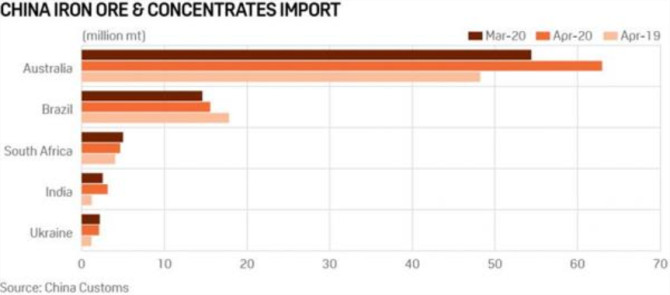

Last year China imported 1.07 billion mt of iron ore, some 60% of which came from Australia and about 20% from Brazil. Seaborne iron ore supply in the January-March quarter is usually affected by seasonal bad weather in the two iron ore producing countries. Iron ore shipments then catch up in the second quarter and are particularly strong in June as this is the last month of the Australian financial year when miners look to optimize revenues. Normally, prices are weaker in June as the rainy season in parts of China slows construction work and crimps demand. But in this abnormal year, iron ore prices could be stronger than usual. Many companies in China want to make up for lost time during February and March and are working harder than normal. Some construction sites are operating around the clock.

Brazil supplies a high grade iron ore product containing low alumina (a chemical in iron ore) that is much sought after by steel mills looking to maximize output and control emissions. But Brazil has a growing number of coronavirus cases which has partially restricted its ability to mine and ship iron ore. Brazilian company Vale has also been recovering from a disaster at a mining waste dam early last year. It may take the company – which is the world’s largest producer – a couple of years to get back to production levels of 2018.

After the massive iron ore capacity expansions in Australia over the past 12 years or so, along with new mines in Brazil, iron ore prices were expected to fall back to modest price levels as supply outstripped demand.

Majors, Rio Tinto and BHP predicted China would produce 1 billion mt/year of crude steel by 2025-2030. Few shared this view; particularly those who accused the large iron ore producers of flooding the market through excessive expansion and hurting iron ore prices.

As it turned out, Rio and BHP were 5-10 years too late – as China produced close to 1 billion mt of steel in 2019, driving demand for raw materials. New steel capacity was also coming on in Southeast Asia. Conversely, Japan and South Korea have been removing steelmaking capacity – and there is a chance some of it may never be switched back on. India has added a lot of steel capacity in recent years and is now the world’s second-largest steel producer – but the country largely depends on its own iron ore reserves, and also exports some iron ore, including to China.

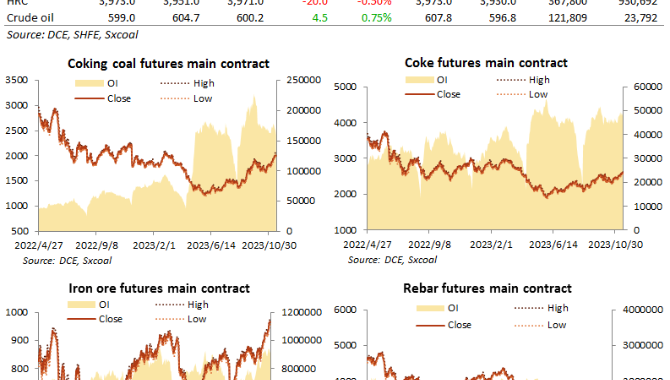

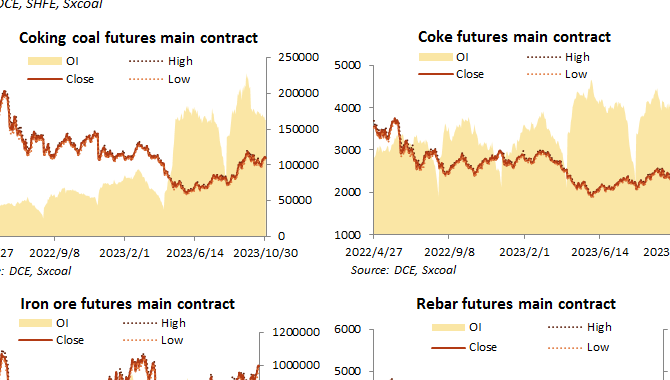

In short, iron ore supply is far tighter than expected and operational issues at mines and ports in Australia and Brazil can have a significant impact on iron ore prices.

Source:Platts

The opinions expressed herein are the author's and not necessarily those of The Xinde Marine News.

Please Contact Us at:

media@xindemarine.com

.gif)

PIL launches Academy to strengthen workforce compet

PIL launches Academy to strengthen workforce compet  Coal shipments to advanced economies down 17% so fa

Coal shipments to advanced economies down 17% so fa  China futures market updates at close (Nov 14)

China futures market updates at close (Nov 14)  CISA: China's daily crude steel output down 5.7% in

CISA: China's daily crude steel output down 5.7% in  China futures market updates at close (Oct 31)

China futures market updates at close (Oct 31)  CISA: China's daily crude steel output down 1.2% in

CISA: China's daily crude steel output down 1.2% in