Steel and raw material prices in China tumbled this week, with iron ore being particularly hard-hit. During Monday’s trading, the 62% Fe benchmark dropped 6% on the day to under $65 per tonne for the first time since July. Although prices seem to have stabilised at $66.4 per tonne today, they are still down almost $10 in a week.

We cannot identify a single apparent reason for the recent sell-off. At this stage, there is also no evidence of a significant, synchronised shift in the broader drivers of steel demand; key steel intensive sectors of property, infrastructure and manufacturing as well as the credit markets are stable.

So, what triggered the sell-off? Probably a range of factors; recent drop in steel prices, concerns over margins, and expectations of steel production cuts are the likely drivers.

Steel prices have been falling for some weeks, partly due to the seasonal factors and partly due to the softening sentiment on the back of slowing industrial activity. By contrast, iron ore prices, especially the 62% Fe benchmark remained remarkably stable for most of 2018 and steadily rose from the beginning of September (please refer to our ATTP dated 15 Nov 19 for a detailed discussion).

With steel prices falling and raw material costs remaining stable/rising, margins came under pressure. Fading profitability and expectations of a drop in production are likely to have fuelled the sell-off.

The other factor which we believe has contributed to the pessimism is the rising pollution levels. We are three weeks into China’s heating season, and there’s been surprisingly little news of production cuts. However air quality has been deteriorating with PM2.5 index levels* climbing well above last year’s levels. Hebei, being a major steel hub, is once again the worst performer. So pressure has probably emerged to curb production which in turned dented sentiment in the iron ore market and contributed to the sell-off.

While the above factors could justify the recent sell-off, they are mostly short-term events. At this stage, there is no evidence of a major shift in macro fundamentals in China, and we regard these sharp moves in prices as a general seasonal weakness and sentiment-driven.

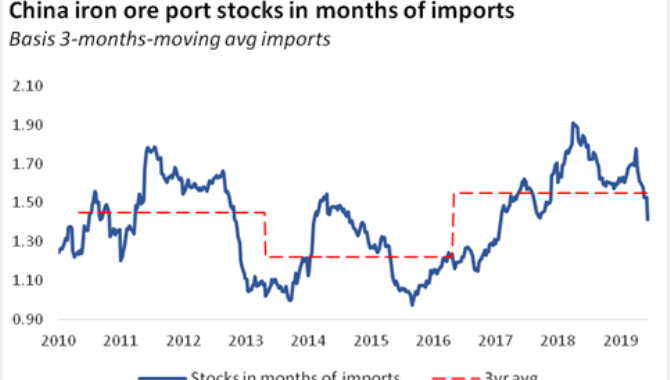

Furthermore, the sharp fall in input costs is positive as it is likely to ease the margin squeeze in the coming weeks. The fall in margins also prompted mills and traders to destock and is currently helping to normalise port stocks that remained stubbornly high throughout the year.

Source:Arrow

Please Contact Us at:

admin@xindemarine.com

.gif)

PIL launches Academy to strengthen workforce compet

PIL launches Academy to strengthen workforce compet  Coal shipments to advanced economies down 17% so fa

Coal shipments to advanced economies down 17% so fa  China futures market updates at close (Nov 14)

China futures market updates at close (Nov 14)  CISA: China's daily crude steel output down 5.7% in

CISA: China's daily crude steel output down 5.7% in  China futures market updates at close (Oct 31)

China futures market updates at close (Oct 31)  CISA: China's daily crude steel output down 1.2% in

CISA: China's daily crude steel output down 1.2% in