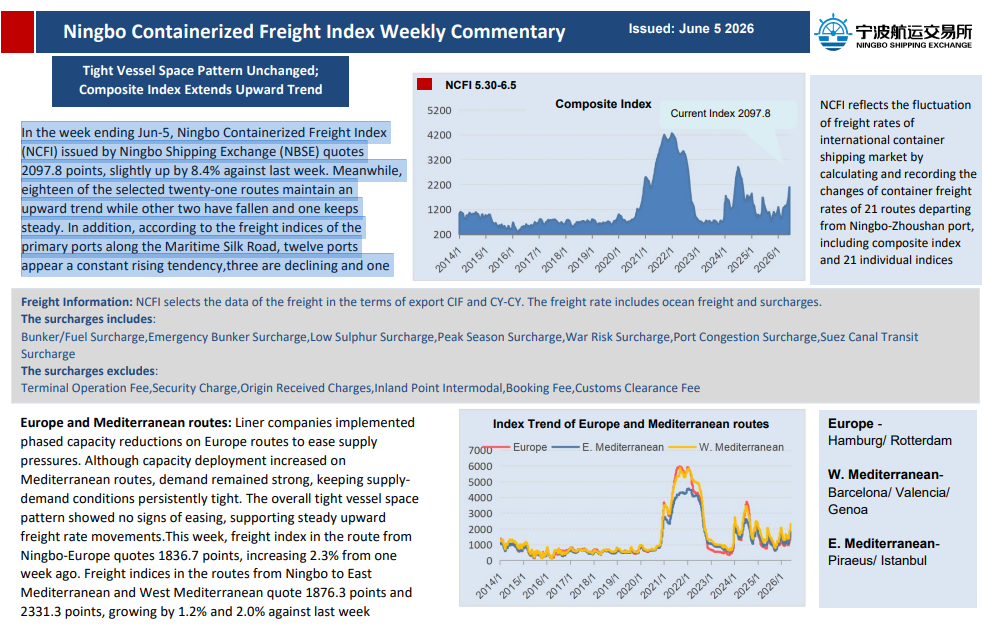

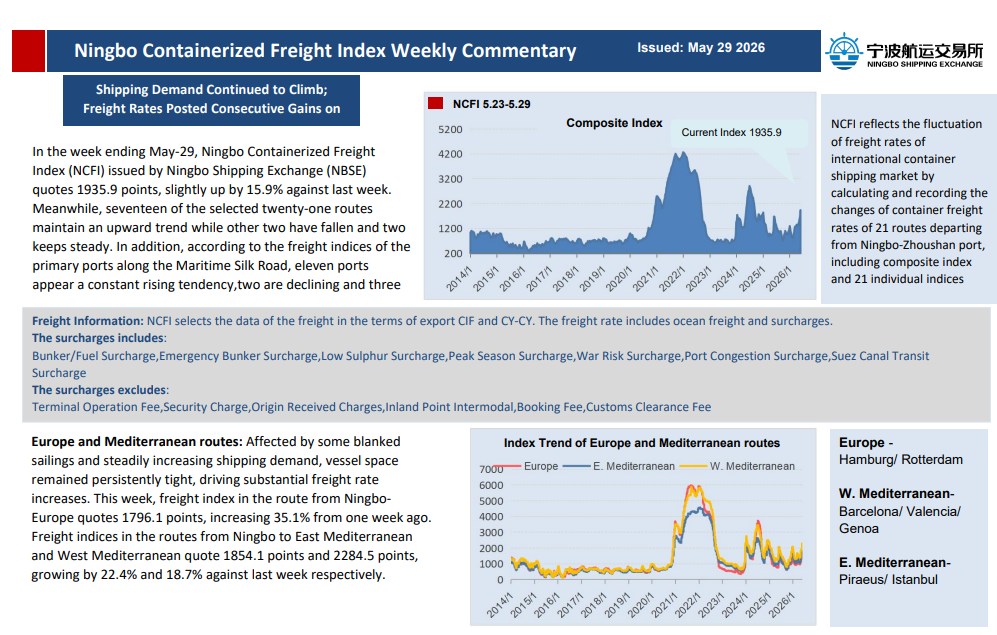

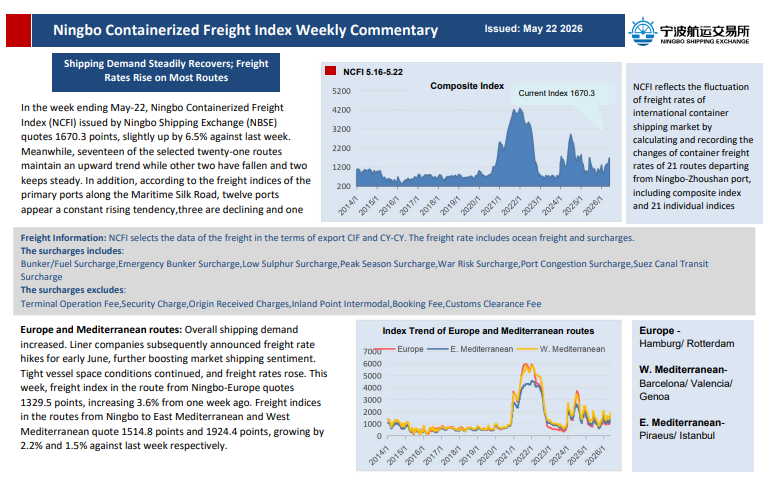

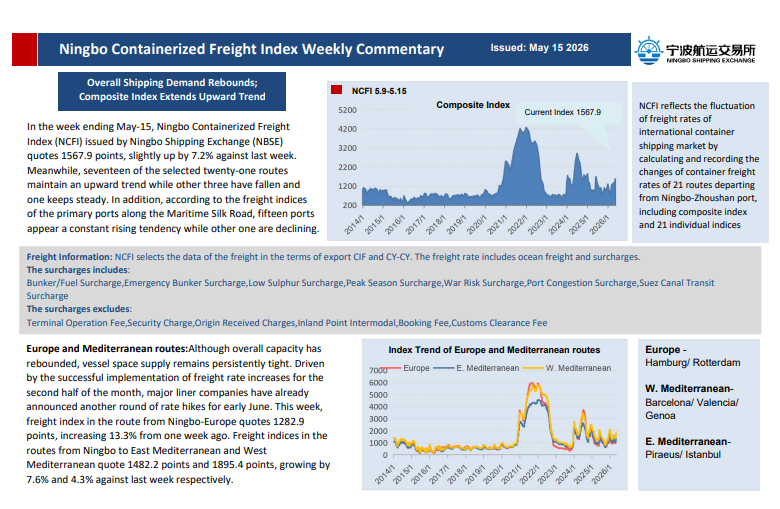

At a time when most shipping conversations are dominated by tankers, energy security and geopolitics, one panel at the recent Capital Link Singapore Maritime Forum made something very clear: dry bulk is back at the center of the global shipping conversation. The discussion brought together Dimitrios Koukas of Optima Shipping Services as moderator, alongside James Marshall of Berge Bulk , John Su of Erasmus Shipinvest Group , Martin Fruergaard of Pacific Basin, Khalid Hashim of Precious Shipping Public Company Limited , and Stamatis Tsantanis of Seanergy. Together, they offered a strikingly constructive — though not simplistic — view on the outlook for dry bulk markets through the rest of 2026 and into 2027. Singapore Maritime Week (SMW)

What stood out was not just that the panel was bullish. It was why they were bullish. Their optimism was not built on a single cargo, a single region, or a single ship type. Instead, it came from several forces working at the same time: limited fleet growth, an aging vessel base, continued geopolitical and canal disruption, resilient grain demand, renewed coal demand linked to energy substitution, and structural ton-mile growth from West African bauxite and Simandou iron ore.

Martin Fruergaard of Pacific Basin Shipping Limited was direct from the outset: in his view, the market remains sustainable. Speaking from the perspective of the smaller dry bulk segments, he argued that even after the temporary hesitation that followed the March conflict escalation, cargo demand has come back as inventories are rebuilt. He also pointed to a strong forward paper market for the balance of the year and into 2027. For Martin, the combination of energy shortages, stronger South American grain crops, possible limits on Ukrainian grain exports, and persistent operating disruptions creates a favorable backdrop for the Handysize, Supramax and Ultramax segments. He also noted that Panama Canal waiting times for ships of this size had stretched to 35–40 days, with transit costs above $1 million, which in itself adds inefficiency and ton-mile support to the market.

If Martin represented the smaller ship segments, @James Marshall and Stamatis Tsantanis pushed the discussion toward the structural strength of the Capesize market. Marshall argued that fleet growth at the larger end has been minimal so far, while demand continues to receive support from additional Brazilian iron ore and surging West African bauxite exports. He described bauxite as one of the biggest structural changes in dry bulk today, noting that the increase in West African volumes is generating major ton-mile demand. He also said Simandou is moving from long-term story to real cargo growth. Based on those fundamentals, he suggested that Capesize earnings should not be below $50,000 per day.

Tsantanis took the Capesize argument even further. His core point was that the real driver today is not demand alone but supply. In his assessment, the Capesize segment is experiencing one of the tightest supply backdrops in the last 20 to 25 years. He pointed to an orderbook of only around 8%–12% of the fleet and an average fleet age of roughly 15 years. That means that over the next three to four years, a significant portion of the existing fleet will either require major capital spending to remain commercially competitive or will need to be replaced. In his view, this supply-side scarcity is the biggest reason the segment remains compelling. He made that view explicit by saying Seanergy would still be willing to order more newbuildings if 2027 delivery slots were available.

One of the most interesting parts of the discussion was the contrast between Capesize and Panamax/Kamsarmax. Zhongyi (John) Su , whose core fleet exposure is in Panamax and Kamsarmax rather than Capesize, did not dispute the strength of the larger ships. But he offered a different lens for the medium-sized market: grain. He argued that grain demand keeps growing because population keeps growing and livestock still needs feed. That makes grain one of the most durable cargo stories for Panamax and Kamsarmax tonnage. At the same time, he said only a limited number of Japanese and Chinese yards are building these vessels, which keeps deliveries restrained. For him, the medium-sized dry bulk market remains a strong long-term proposition, especially from Ultramax up to Kamsarmax.

That point matters because it shows that this is not a one-dimensional market. Capesize strength is being driven by iron ore, bauxite and supply scarcity. Panamax and Kamsarmax strength is being supported by grain, trade resilience and still-disciplined fleet growth. In other words, different parts of the dry bulk market are strong for different reasons — and that makes the broader rally more convincing.

Coal, unsurprisingly, became another key topic. The panel acknowledged the irony openly. A decade ago, coal was being written off by many as a cargo that would gradually disappear from shipping. Today, it is back as one of the most important balancing factors in global dry bulk. Tsantanis argued that the recent energy shock has reopened coal’s role as a substitute fuel, particularly in Asia, where he estimated coal-fired energy demand could increase by 40–60 million tonnes in 2026 if current conditions persist. In his view, if energy markets do not normalize quickly, coal demand could continue to support freight markets for another six to nine months.

John Su added a longer-cycle perspective. He recalled the deep market trough when the BDI fell to around 290 and coal was condemned by many as a “dirty cargo” with no future. Yet, as he pointed out, dry bulk is still here — and coal remains indispensable in many developing economies. His point was not ideological. It was practical: the energy transition is not linear, and in the real world, coal is likely to remain a meaningful cargo for years to come.

Marshall then returned to what may be the most important structural trade shift in dry bulk today: West Africa. He emphasized that the increase in bauxite exports from the region is already reshaping ton-mile demand. He also highlighted Simandou as a future game changer, saying that while current volumes remain limited, cargoes should ramp up significantly next year and could exceed 100 million tonnes by the end of the decade. At the same time, Marshall offered an important note of caution: the market already has around 275 Capesize newbuilding orders on the books, and over time those deliveries could be enough to cover the incremental demand created by Simandou. In other words, Simandou is bullish — but not a one-way story. It will attract supply as well as demand.

That caution is important because it distinguished Marshall’s position from the most aggressive newbuilding bulls. He was constructive on the market, especially for Capesize, but not blindly so. His closing investment answer was not “order more ships at any price.” Instead, he emphasized two priorities: continue improving the efficiency of the existing fleet and continue investing in climate technology. That is a very different message from a simple expansion call.

The panel’s discussion on newbuilding strategy was one of its most revealing sections. Tsantanis was the most open about still wanting newbuildings, provided delivery slots could be secured. John Su was much more cautious, not because he doubts the market, but because he believes current asset prices are high and debt repayment capacity must come first. Martin Fruergaard took a similarly disciplined view, saying assets are expensive and hard to justify outright. Pacific Basin, he noted, has around 10 ships in its pipeline, but more through long-term leasing with purchase options than through aggressive direct asset accumulation. Khalid Hashim described a different strategy again: Precious Shipping has added nine Ultramaxes in the past six months, mainly through resales and secondhand acquisitions, rather than by waiting for distant yard slots.

Taken together, these comments say a lot about the current investment climate in dry bulk. Most owners agree that future tonnage matters. But the real constraints today are yard availability, elevated prices, delivery timing, regulation uncertainty, and whether returns can justify the capital committed. This is not a market where owners are uniformly rushing to order. It is a market where almost everyone sees value in future exposure, but each is choosing a different path to get there.

The decarbonization discussion added another layer. Marshall said Berge Bulk remains disappointed by delays in the IMO framework, but the company is not waiting for regulation to become perfect. He outlined a three-part roadmap: make the legacy fleet more efficient, use new fuels, and adopt new technologies. He said Berge Bulk has already completed a 100% biofuel voyage test and is also looking at wind-assisted propulsion technologies such as rotor sails.

@Khalid Hashim provided one of the most pragmatic interventions of the panel. Precious Shipping operates mainly in the geared sector, and he explained that many of the more visible decarbonization technologies do not fit easily on those vessels. Instead of betting heavily on future fuels that may not be available in remote ports, the company’s focus has been on lowering fuel consumption as much as possible and rejuvenating the fleet. He noted that Precious Shipping’s average carbon intensity has dropped from 12.55 in 2014 to 5.5 today, a reduction of more than 50%, helped in part by replacing older non-electronic-engine ships with more efficient electronically controlled engine vessels.

Tsantanis added another frustration from the owner side: charterers are not always willing to share the cost of efficiency investments, even when those investments clearly reduce fuel burn. He mentioned cases where vessel improvements such as silicone coatings could cut fuel consumption by 10%, yet charterers were still reluctant to contribute. Martin Fruergaard countered that Pacific Basin’s voyage-heavy operating model makes it easier for the company to capture the benefit of its own investments. That is one reason why Pacific Basin is putting significant effort into digitalization, machine learning and speed optimization rather than simply spending more on aging ships.

The final question of the panel asked what investment decision each executive would make today if judged five years from now. The answers were revealing. Tsantanis chose newbuildings. Khalid chose resales and secondhand Ultramaxes. Marshall chose efficiency upgrades and climate technology. John Su chose grain-related business and the medium-sized vessel classes from Ultramax to Kamsarmax. Martin chose people — both at sea and ashore — arguing that talent will remain the most decisive competitive factor in running a fleet well. The moderator closed that thought with a reminder that the world will need around 800,000 more seafarers in the next five years.

That, perhaps, was the most useful takeaway of the session. This is not just a freight market story. It is not just a cargo story. And it is not just a fleet supply story. It is a market where several structural forces are reinforcing each other at the same time: aging tonnage, selective ordering, changing commodity flows, energy substitution, canal inefficiencies, geopolitical rerouting and the long shadow of the energy transition.

So how long can this dry bulk rally last?

If this panel is any guide, the answer is: longer than many expected — but not for simple reasons. Capesize is being supported by supply scarcity and long-haul mineral trades. Panamax and Kamsarmax are underpinned by grain and resilient medium-sized cargo demand. Coal has re-emerged as an uncomfortable but undeniable support factor. Bauxite and Simandou are reshaping ton-mile patterns. At the same time, high asset prices, an eventual orderbook response, port bottlenecks, and fragmented decarbonization economics remain real risks.

The message from Singapore was therefore not “everything is easy.” It was something more valuable: dry bulk is entering a period of structural repricing, and the winners will be those who can think more carefully than the market about ship type, cargo mix, asset timing, coverage strategy, and technology path.

The opinions expressed herein are the author's and not necessarily those of The Xinde Marine News.

Please Contact Us at:

media@xindemarine.com