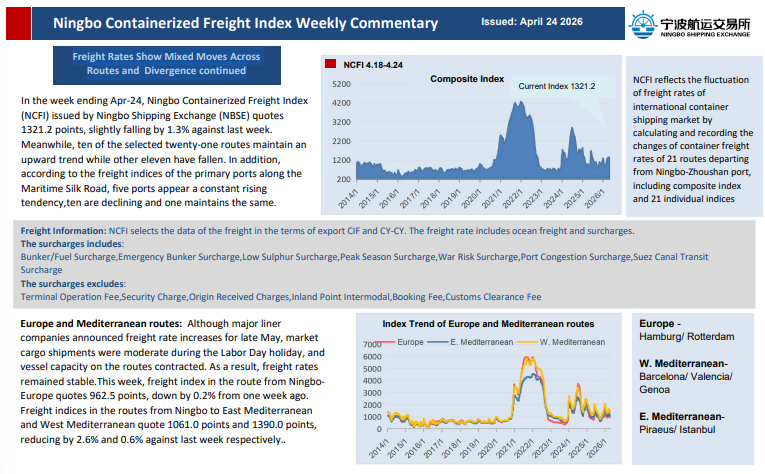

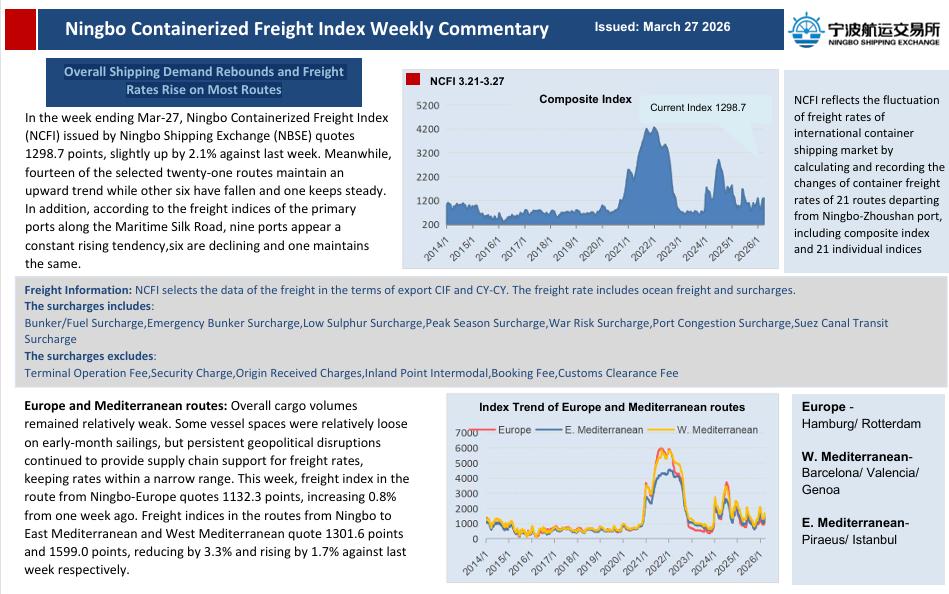

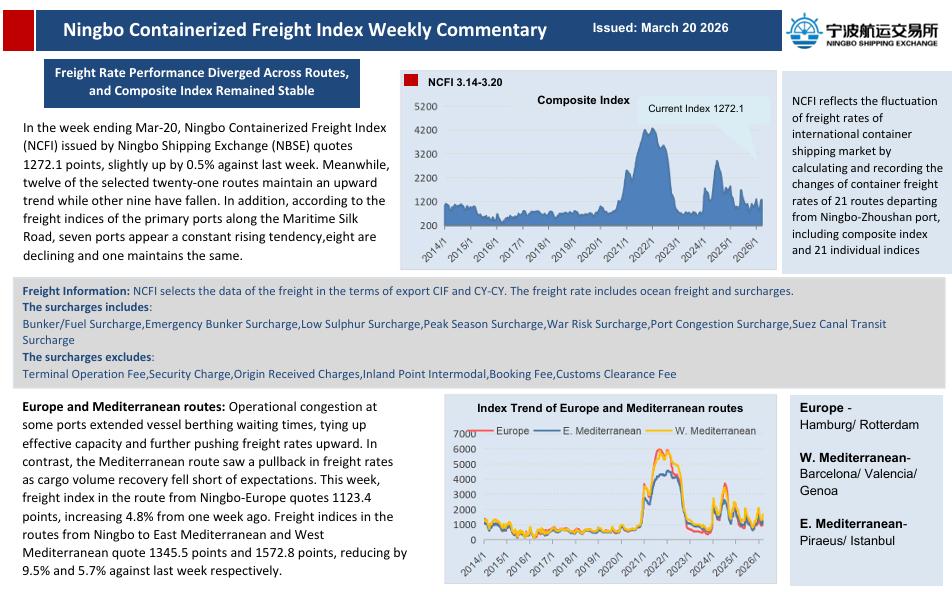

The container shipping industry has shown impressive resilience through years of volatile energy prices, disrupted trade flows, and persistent geopolitical shocks. Yet much of that resilience has been defensive—built on rapid operational adjustments, rerouting, and risk management—rather than on decisive, large-scale investment in new technology. Under the banner of “green transition,” the sector is now facing a growing mismatch: regulatory ambition is accelerating, but technology readiness, bunkering infrastructure, and financing solutions are not progressing at the same pace.

In an article published by the Greek media outlet NAFTEMPORIKI, Contships Management Inc COO Angelos Tyrogalas makes a sharp observation: when uncertainty becomes the dominant condition, markets are pushed to adapt rather than empowered to innovate. That point matters, because it highlights a risk the industry is still underestimating—one that sits in plain sight inside the container network.

Newbuilding Reality: "More Expensive and Slower" Means Less Appetite for Technology Bets

Over the past few years, newbuilding prices have risen sharply, while yard capacity has tightened and delivery schedules have extended into the late 2020s. This combination makes the classic shipping investment equation harder: owners must commit capital today for assets that will deliver years later, under market, fuel, and regulatory conditions that are increasingly difficult to forecast.

Under these circumstances, shipowners naturally prioritize investments with clearer, more bankable returns. When alternative fuel pathways remain uncertain and their commercial payback is harder to model, "technology premiums" become more difficult to justify—especially outside of the largest, best-capitalized fleets.

This is where the real vulnerability emerges: feeder and regional tonnage. Compared with mainline vessels, feeders typically have thinner margins, shorter trade cycles, and less ability to absorb higher capex or operational constraints. As a result, they are more likely to rely on incremental compliance and optimization, rather than taking early-stage innovation risk.

The "Feeder Gap": A Data Signal the Market Should Not Ignore

If we define feeder container ships as below 4,000 TEU, Clarkson Research data for 2025 global newbuilding orders shows that feeder ordering activity was substantial—296 vessels in total. Yet only 47 vessels (15.9%) were recorded with any form of alternative fuel / new energy notation in the dataset (including “Ready” and propulsion alternatives). Most of the remaining feeder orders—249 vessels (84.1%)—did not indicate a green fuel or new energy configuration.

The picture becomes even more striking when applying a stricter definition: if we exclude all “Ready” notations and count only "Capable" ships as true alternative fuel tonnage, then feeder orders with new energy capability shrink to just 8 vessels, or 2.7% of the total—essentially all LNG-capable.

In other words: the overwhelming majority of feeder orders last year did not commit to "capable" alternative fuel solutions. The industry may be progressing on decarbonization narratives at the top end of the fleet, but the numbers suggest a quiet lag where it matters operationally: the feeder network that connects hubs to regional ports.

Why This Matters: Three Layers of Uncertainty That Keep Innovation on Hold

Tyrogalas's argument is not that owners oppose decarbonization. The deeper issue is that the system is not yet engineered to support confident innovation decisions. Three forms of uncertainty stack up:

Fuel economics remain unstable. Alternative fuels can carry significant price premia, and their long-term supply dynamics are still evolving. Without a stable cost outlook, shipowners cannot build reliable cash-flow models.

Bunkering infrastructure remains uneven. Shipping is a network business, and feasibility depends on port capabilities. Even if large hubs move first, many secondary and regional ports—where feeders spend much of their operating life—may not offer the same fuel availability or logistics maturity. That directly reduces operational flexibility.

Carbon pricing and regulation are fragmented. Global mechanisms are still under debate, while regional policies are already active. This creates compliance complexity, uncertain cost pass-through, and shifting incentives—conditions that naturally push capital toward short-term, low-regret adaptations instead of long-term innovation bets.

The Structural Risk: Mainline Upgrades vs. Feeder Lock-In

A two-speed transition is emerging. Larger owners and mainline services have greater ability to invest in dual-fuel newbuilds and to secure longer-term commercial structures to justify higher capex. Meanwhile, feeder operators—constrained by financing, infrastructure realities, and weaker cost absorption—risk being locked into conventional designs.

But feeders are not a marginal segment. They are the "capillaries" of the container system. If feeder fleets lag for too long, the industry's overall emissions reduction trajectory will face a structural bottleneck. And when regulatory pressure intensifies, the exposure may surface suddenly: higher compliance costs, reduced service competitiveness, asset value volatility, and operational disruption—especially in regions where alternative fuel infrastructure remains limited.

A Core Message: Decarbonization Is Not an Excel Exercise

One of the most practical takeaways from Tyrogalas is that decarbonization cannot be achieved through taxation or compliance checklists alone. Regulation can set direction—but without credible technology pathways, port readiness, and finance mechanisms, the market will default to defensive behavior: optimize what exists, delay what is uncertain, and adopt what is easiest to justify.

Shipping is a capital-intensive industry with long asset lives. If policy signals, fuel pathways, and infrastructure buildout remain unpredictable, it is rational—not irresponsible—for many owners to prioritize balance-sheet safety over innovation risk. The result, however, is exactly what Tyrogalas warns about: innovation is delayed, adaptation is accelerated, and transition becomes reactive rather than strategic.

A Practical Path Forward: Certainty, Finance, Infrastructure, and Reinvestment

If the goal is to shift the market from "forced adaptation" to real innovation, the solution must be more engineering-driven and less slogan-driven:

Provide clearer long-term signals—especially on carbon pricing. Investors and owners need a stable framework to price risk and reward.

Design financing tools that fit feeder realities. Smaller and regional fleets cannot be expected to carry the same transition burden as mainline giants. Risk-sharing mechanisms and tailored capital structures matter.

Synchronize fleet requirements with port readiness. Before demanding "ready" ship specs at scale, supply chains and port networks must be prepared—particularly across the regional ports feeders depend on.

Recycle decarbonization revenues into R&D and infrastructure. If carbon-related costs do not flow back into technology development, bunkering networks, and shore-side upgrades, they will not produce system capability—only system friction.

Closing Thought

The container market’s hidden risk is not only about technology—it is about transition architecture. Angelos Tyrogalas’s point is simple but powerful: when uncertainty dominates, markets adapt to survive, but they do not innovate to transform.

Clarkson’s feeder ordering data adds a hard signal to that argument: under a strict "capable" definition, only 2.7% of feeder orders last year committed to alternative fuel capability. If feeders remain the weak link, the industry’s decarbonization pathway will be constrained by its own network design.

A credible transition requires more than ambition. It requires executable pathways: certainty that reduces risk, financing that matches fleet segments, infrastructure that enables operations, and reinvestment that builds real capability. Without these, we should not be surprised if the market keeps adapting—because it was never given the conditions to innovate.

Please Contact Us at:

media@xindemarine.com