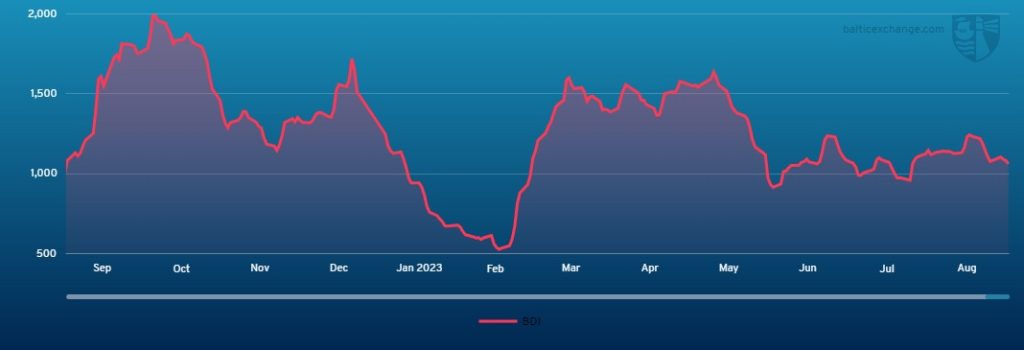

Capesize

The Capesize market observed a shortened trading week due to the public holiday in the UK on Monday and another in Singapore on Friday. Trading in the Pacific region displayed consistent volumes throughout the week. The presence of all three major players led to a slightly optimistic market sentiment earlier in the week, but this positivity did not significantly impact rates on C5, which saw only a minor increase. Meanwhile, the Atlantic market remained subdued, with bids on C3 struggling to attract interest, reflecting owners’ hesitancy. The North Atlantic faced challenges with an excess of spot vessels and a shortage of cargo, pressuring the market. Despite hopes for increased Pacific activity before Singapore’s holiday on Friday, the market did not experience a significant upswing, and freight rates remained relatively steady. The North Atlantic continued to grapple with oversupply issues, leading to limited enquiry and competition among owners for available cargoes. Rates from South Brazil to the Far East experienced further declines as charterers adjusted their bids downward. Overall, the market sentiment persisted as bearish.

Panamax

The Panamax market opened the week on a firm footing, but we ended with rates slowly eroding, particularly in the Atlantic as pressure was applied all week with a basic lack of demand, especially for the Transatlantic trades. South America front haul trips started brightly but activity fizzled out as the week progressed, with several deals concluding mid-week basis delivery India at $16,000. Conversely, Asia witnessed solid cargo volumes ex Australia and NoPac, including an 82,000-dwt delivery North China fixed for a NoPac round trip at $12,000. Some impacts being applied by a typhoon in the south of the region, the market with favourable positioned ships taking advantage. However, nervousness from the Atlantic physical and FFA market appeared to impact the basin here too as we approached the weekend. Period activity remained minimal with a wide bid/offer spread but reports of a scrubber-fitted 81,500-dwt delivery Hong Kong achieving $11,000 basis 6/8 months.

Ultramax/Supramax

Gains were seen this week across the Atlantic as demand increased and limited tonnage availability was evident. The Black Sea region was especially active with a 61,000-dwt fixing from Eregli via the Black Sea to Singapore-Japan range at $20,500. In the US Gulf, a 63,000-dwt was fixed for a trip to India at $22,000 whilst a 61,000-dwt fixed from Brownsville to Egypt at $18,750 with a guaranteed minimum duration of 50 days. The South Atlantic also improved with a 62,000-dwt fixing from San Nicolas to Singapore-Japan range at $16,000 plus a $600,000 ballast bonus. Increased activity in the Indian Ocean was also evident, with a 60,000-dwt fixing from Cape Town via Saldanha to China at $17,500 with a $175,000 ballast bonus. In Asia, levels were more balanced with a holiday in Singapore tempering activity, a 61,000-dwt fixed from Gresik to WC India at $14,500. Period activity remained and a 63,000-dwt opening in India fixed 4 to 6 months at $15,000.

Handysize

The Handy sector has remained positive, with the Atlantic seeing the biggest gains. In the Black Sea, a 35,000-dwt was fixed passing Canakkale via Constantza to Jebel Ali at $10,000 whilst a 34,000-dwt fixed from Otranto via Constantza to Morocco at $12,000. Activity was said to have improved on the North Coast of South America with a 33,000-dwt fixing a trip to the Continent at $9,000. A 37,000-dwt fixed an Alumina cargo from Fazendinha to Norway at $16,000. The Asia markets were more balanced. A 32,000-dwt was fixed from Singapore via Australia for a round voyage at $9,500 whilst a 35,000-dwt opening ex dry dock in China fixed a trip via Japan to the East Coast of India with steels at $9,500. Period had also been active with a 32,000-dwt opening in China fixing for 4 to 6 months at $9,850, whilst in the Atlantic a 37,000-dwt opening in Brunsbuttle fixed for 7 to 9 months at 95% of the BHSI index.

Clean

LR2

LR2’s in the MEG showed signs of freight level improvement this week. TC1 took a 4.16-point step up to WS134.44 seeing the Baltic TCE of hold in the $27,000/day region). Meanwhile, a run to the UK-Continent on TC20 climbed circa $130,000 to $3,880,000.

West of Suez, Mediterranean/East LR2’s held stable around the $2,950,000 mark.

LR1

In the MEG, LR1’s saw similar incremental freight rises to their larger siblings. The TC5 index ultimately hopped up a modest 3.75 points to WS145 whilst for a trip to the UK-Continent on TC8, ended the week at $3,320,000 (up $156,000).

On the UK-Continent, TC16 improved for the second week on week, climbing 15% this week to WS155.94 (+20.94 points).

MR

MEG MR’s took a sharp retest back down this week coming under repeated pressure during the week. The TC17 subsequently shed 25 points to WS249.29. UK-Continent MR’s improved consistently through this week assisted by the notably strong Mediterranean market. TC2 rose to WS223.75 (+12.25) and similarly TC19 is currently pegged at WS233.13 (+10.94). This took the TC19 Baltic round trip TCE back over the $30,000/day level.

USG MR’s returned to a firmly upward course this week off the back of high fixing volume. TC14 returned back to WS144.58 after bottoming out at WS130 and TC18 followed an identical pattern flooring at WS230 to return to WS238.33 at time of writing. A voyage to the Caribbean on TC21 returned to $991,000 after reaching a nadir of $770,000.

The MR Atlantic Triangulation Basket TCE climbed from $34,521 to $35,720.

Handymax

In the Mediterranean, Handymax’s look to have hit the ceiling with the TC6 index topping out at WS279.56 is currently marked at WS267.5. Up on the UK-Continent, the TC23 index ticked up 6.67 points to WS192.5.

VLCC

The market in the Middle East slid down once again this week, although much of the deals concluded are on ‘compromised’ vessels either ex dry-dock, lacking an updated SIRE report or over-aged. It remains to be seen whether owners of non-‘compromised’ vessels can fare any better, thus far showing a lack of desire to compete. The rate for 270,000 mt Middle East Gulf to China lost four points to WS39.71 corresponding to a daily round-trip TCE of $10,173 basis the Baltic Exchange’s vessel description. The 280,000 mt Middle East Gulf to US Gulf trip (via the cape/cape routing) was assessed 1.5 points lower than a week ago at just below WS25.

For the Atlantic market, the 260,000 mt West Africa/China rate was reduced by 3.5 points to WS47.9 (which shows a round voyage TCE of $22,300/day). The rate for 270,000 mt US Gulf/China was reduced by $927,777 to $7,466,667 (about $24,500/day round trip TCE).

Suezmax

Suezmaxes in West Africa had another poor week and, although a number of ships have been quietly picked off by charterers, there is still not enough activity here (and in surrounding markets) for owners to get a decent grip on rates, facing persistent over supply of tonnage. Rates overall dropped about five points for the 130,000 mt Nigeria/Rotterdam trip to WS70.45 (a daily round-trip TCE of $16,000). In the Mediterranean and Black Sea region, there has been a little more interest in voyages to the east, but it is not enough to reverse the recent downward trend for the 135,000 mt CPC/Med route, and the panellists last assessed TD6 two points lower than a week ago at WS71.70 (showing a daily TCE of about $8,300 round-trip). In the Middle East, the rate for 140,000 mt Basrah/Lavera eased two points to WS57.33.

Aframax

In the North Sea, the rate for the 80,000 mt Hound Point/Wilhelmshaven route slipped two points to WS105 (showing a round-trip daily TCE of $9,800) despite the return of a busier Russian Baltic export programme for the first 10 days of September (reported to be 2.2 million tonnes, compared to 1.6 million for the first 10 days of August). In the Mediterranean market the rate for 80,000 mt Ceyhan/Lavera shed four points to WS102.33 (a daily round trip TCE of $14,500).

Across the Atlantic, in the Stateside Aframax market, the roller-coaster ride is back in effect but with shallower peaks and troughs than we have seen earlier this year. The rate for 70,000 mt East Coast Mexico/US Gulf fell nine points to WS120.63 (which shows a TCE of $17,450/day round trip) and for 70,000 mt Covenas/US Gulf, the market rate has had about six points taken out of it, to WS113.75 (a round-trip TCE of $15,500/day). The rate for the trans-Atlantic route of 70,000 mt US Gulf/Rotterdam has also lost about nine points to WS114.38 (a round trip TCE of $18,100/day).

LNG

It has been another positive week on rates for LNG with the index rising on all three routes. Despite some activities in fixing out in the Pacific, the rise is more in line with market expectations for October/November laycans and the potential for winter spikes in spot rates rather than physical drivers. BLNG1g Aus-Japan rose by $22,308 to close at $144,045/day for a round voyage. There are still concerns that industrial action in Australia will have an effect, but it seems more to be on the product side than the freight and the overall impact is yet to be realised. Sentiment and brokers are showing expectant signs of life and hope that the winter brings with it again a rise in rates, and some liquidity.

For BLNG2g US-Cont, the rates rose $26,482/day for a round voyage trip bringing the index to $142,427, while BLNG3g still very much hampered by long and costly (one reported owner, potentially either LNG or LPG, shelled out $2,400,000 at auction to secure transit) delays in the Panama saw a decent jump of $24,434/day to bring the round voyage rate up to $178,637. US LNG exports rose in the week ending 30 August compared to the week before. An increase of around three further stems lifted supports the rise of the index and suggests that terminals and charterers are beginning to ramp up movements.

LPG

A stable start to the week was turned on its head after one charterer went out for a ship that opened the gates for others sitting on stems to rush out to secure any available tonnage. This pushed rates higher by $22.857 on the week with the rise seen pretty much in the last day alone. Rates for Ras Tanura-Chiba closed at $118.143 giving a daily TCE return of $104,137 – this is the highest level seen since end of June where rates were only $1 higher, suggesting there is more to come.

The US market was not quite as meteoric, however positive gains were seen on both routes. BLPG2 Houston-Flushing gained $5 to close at $103.8 with a daily TCE earning of $118,831. This is the highest level seen on the index this year, beating out the previous high of end June by just under $1. The BLPG3 Houston-Chiba was busy with fixing pushing rates up over $12.285 to close at $182.571 and a daily TCE earning of $102,244. Overall, a productive week for brokers and owners alike in a market where rates rose, and enquiries were thin and tentative due to short supply of ships and continued delays in Panama means some are ready to pay higher freight.

Source:

Hong Kong Maritime Hub

The opinions expressed herein are the author's and not necessarily those of The Xinde Marine News.

Please Contact Us at:

media@xindemarine.com

.gif)

Ningbo Containerized Freight Index Weekly Commentar

Ningbo Containerized Freight Index Weekly Commentar  Ningbo Containerized Freight Index Weekly Commentar

Ningbo Containerized Freight Index Weekly Commentar  BIMCO Shipping Number of the Week: Bulker newbuildi

BIMCO Shipping Number of the Week: Bulker newbuildi  Ningbo Containerized Freight Index Weekly Commentar

Ningbo Containerized Freight Index Weekly Commentar  Ningbo Containerized Freight Index Weekly Commentar

Ningbo Containerized Freight Index Weekly Commentar