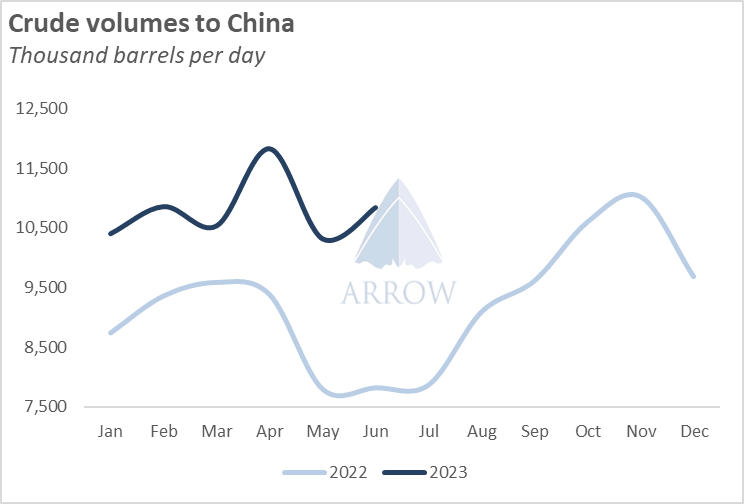

China’s appetite for crude oil has been the major driver for global demand this year, outstripping volumes in 2022, with an average monthly year-on-year increase of 24%. Domestic crude demand has risen, but we expect to see an increase in clean product exports to the Asia Pacific region and potentially further afield as well.

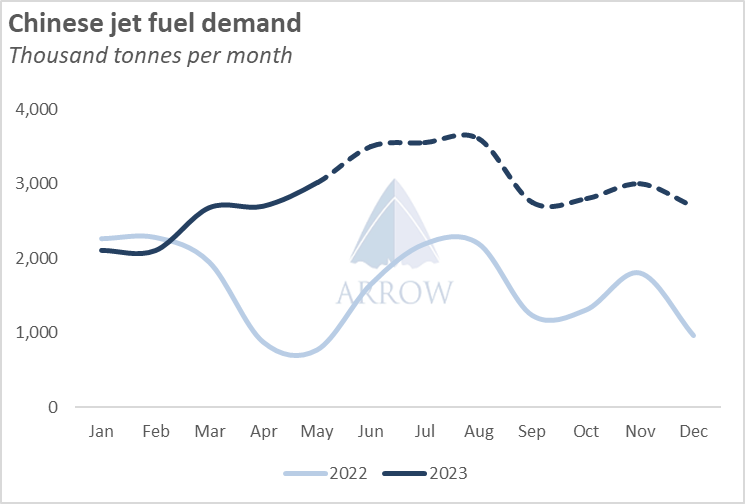

China’s growing demand for Jet fuel has been almost insatiable with refineries optimising to produce middle distillates. However, this has left it with a surplus of other middle distillate products such as gasoil/diesel. China is structurally net long in jet (+1.7 MT/month on avg 2022), gasoline (+1.1 MT/month avg 2022) and gasoil/diesel (+900KT/month avg 2022). These product surpluses are going to increase as capacity grows and should lead to higher exports as crude supply tightens and refining margins improve within the region.

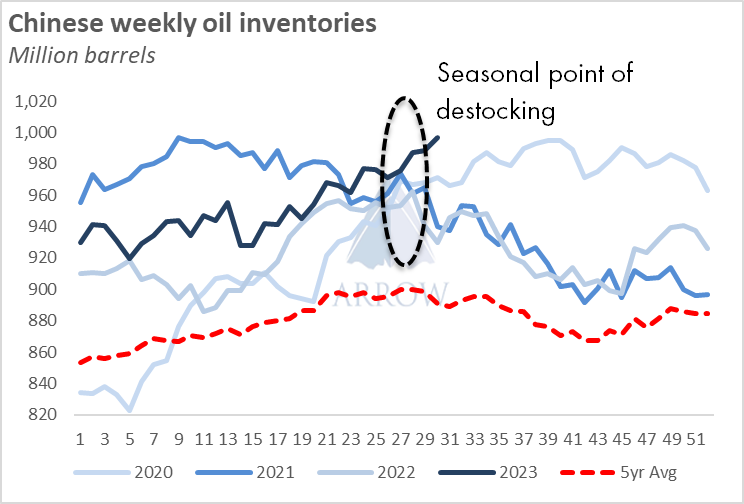

As of today, Chinese refineries are almost entirely out of turnarounds, with a few nationally owned still undertaking maintenance. During the downtime, China stored oil that was not being put through the refineries, while also continuing to take advantage, and stockpile, cheap Russian oil which has a high yield for middle distillates.

This has led to higher inventories, exceeding levels for the past five years. Normally, post maintenance season, we see a gradual decline in inventories, however this has not happened, and the country is even outstripping 2020’s peak pandemic inventory levels. Bearing in mind that the summer season is upon us there is bound to be an increase in domestic utilisation. Crude bought at reduced prices will also give an extra boost to refiners’ margins as demand picks up and exports rise.

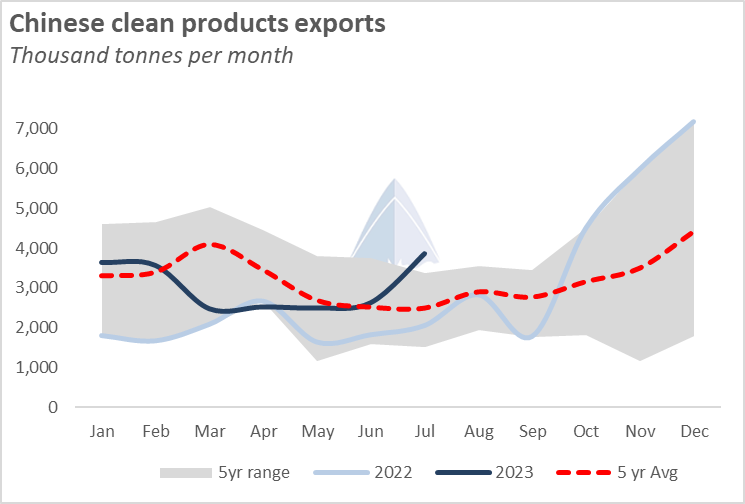

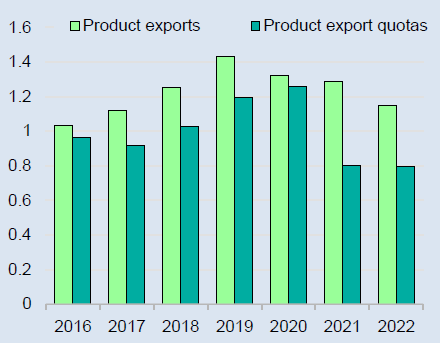

Despite rising domestic consumption in July, we have seen China exporting 60% more clean products on average this year, pushing out of its 5-year range. Higher exports are in part driven by China’s growing refining industry. The additional refining capacity of over 1mb/d since 2020 has meant an increased production of clean products. In addition, exports have historically exceeded the export quotas, which means that there is scope for further increases in exports. Considering the inventory levels, we are likely to see an increase in shipments going forward, specifically in gasoil and diesel which have increased by 98% (+260KT) and 246% (+714KT) respectively for the first 6 months of 2023 compared to the previous year, driven by a surplus from refinery optimisation and rising margins.

Chinese product exports vs quotas

Million barrels per day

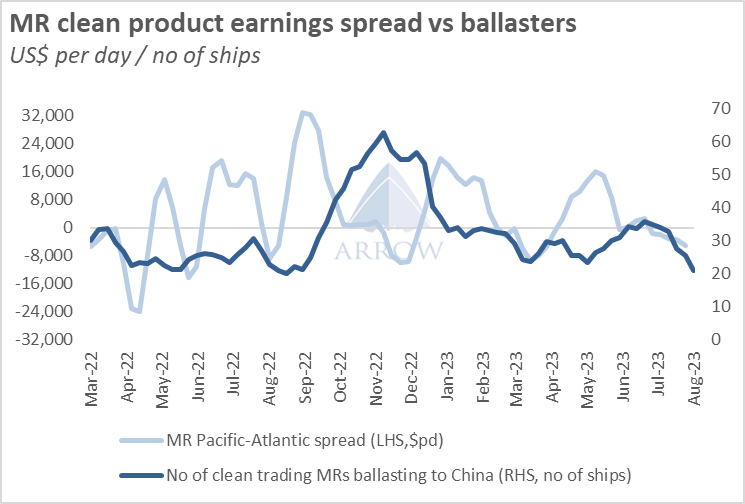

Traditionally MRs have dominated Chinese clean product exports, averaging 57% of total exports in 2022. This has increased to 66% for 2023 YTD. We expect MRs to continue to dominate this trade and benefit from rising volumes in the coming months.

MR Pacific earnings have already seen steady gains recently, increasing from about $15,000 per day in early July to over $25,000 this week. Further gains are likely as tonnage supply in the region is seemingly tightening. Lured by higher rates in the Atlantic, the number of clean trading MR tankers ballasting to China have been falling steadily. This comes at a time when exports are set to rise as China gears up to offload its surplus barrels in the region.

High inventories and structural surpluses are driving Chinese exports higher. With tightening tonnage supply due to falling ballasters, the MR outlook in North Asia is set to be positive over the coming weeks.

.gif)

Ningbo Containerized Freight Index Weekly Commentar

Ningbo Containerized Freight Index Weekly Commentar  Ningbo Containerized Freight Index Weekly Commentar

Ningbo Containerized Freight Index Weekly Commentar  BIMCO Shipping Number of the Week: Bulker newbuildi

BIMCO Shipping Number of the Week: Bulker newbuildi  Ningbo Containerized Freight Index Weekly Commentar

Ningbo Containerized Freight Index Weekly Commentar  Ningbo Containerized Freight Index Weekly Commentar

Ningbo Containerized Freight Index Weekly Commentar