Signal Maritime examines the impact of clean commodity flows and the new trends coming to freight using data from Signal Ocean

The end of the first quarter of this year brings strength potential for the clean LR2 segment, as the volume of clean flows from east to west has already increased. It appears that the European ban on Russian oil products imposed in February opens the doors for firmness in trade from the Arabian Gulf to the West, supporting the increase in demand in ton-miles, with the pace of ocean shipping peaking in early May as the volume of clean oil flows from the East to Europe increases.

In the crude segment, oil shipments from Russia destined for China and India slowed in April after peaks in the first quarter of this year, and it remains to be seen whether Asian energy demand will continue to feed the Russian oil economy. In the clean segment, AG appears to be playing a critical role in the West, with the size of LR2 tankers benefiting from the current trend in oil shipments to Europe.

Our analysis based on Signal Ocean Data looks at recent developments in market prices, direction of flows, cargo trends, ton-mile demand, supply trends, and ballast speed in knots.

I. Market Rates - LR2 AG

The beginning of the year was disappointing for LR2 tankers, as rates slumped before and after the ban went into effect, but in March and April, rate trends were more optimistic and sentiment was better. Although recent momentum has yet to reach the peak of over 300 WS (image 1) seen late in the fourth quarter of last year, stable sentiment of around 150 WS has been seen recently. Today's supply and demand fundamentals, as well as the volume of clean oil flows, underscore that a collapse similar to the February lows is not likely to occur soon.

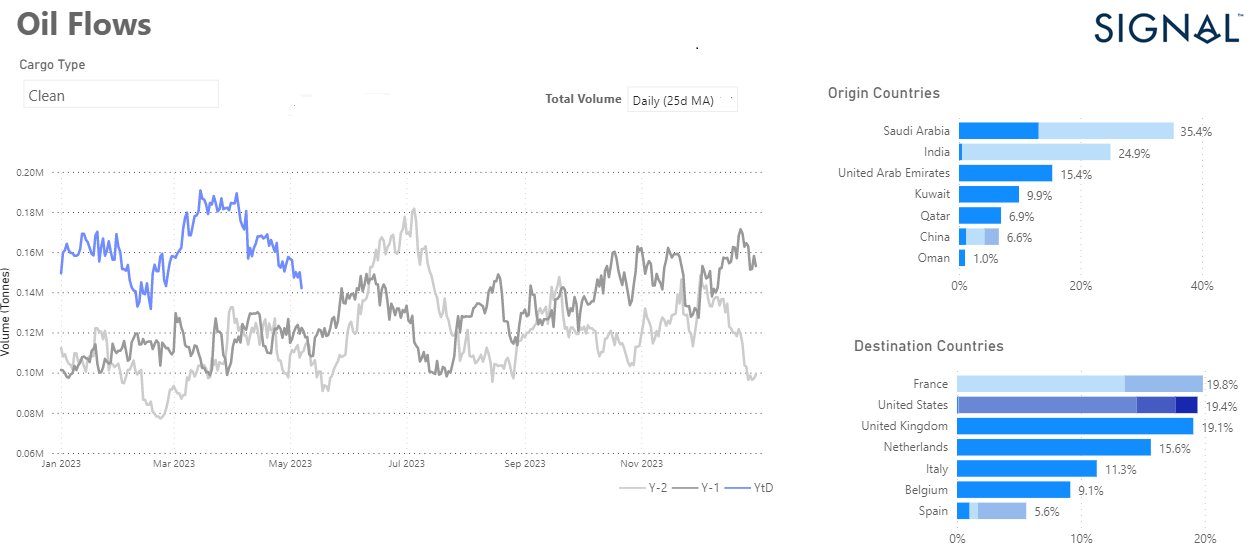

At the beginning of the year, the momentum of clean oil flows from the East to the West weakened, although daily volumes were significantly higher than two years earlier, when the energy industry was not threatened by geopolitical tensions and uncertain Russian oil supplies. As shown in image 2, more clean energy supplies were delivered to the East starting in March, with Saudi Arabia playing a leading role in deliveries to the West. The 25-day moving average is still at a higher level than two years ago, with a downward trend in the last few days, while a peak similar to June/July 2022 could be reached at the end of the second quarter.

Looking at flows of clean petroleum products by origin, expressed in monthly volumes (tonnes) (image 3), we see that Saudi Arabia's share has steadily increased over the past year, approaching a share of over 35% of volumes destined for the West. The second most important source country for the Western countries seems to be the region of India with a share of almost 25%, while other Eastern countries with still significant shares are expected in the region of Pakistan/West Coast of India.

The destinations of clean flows to the West are primarily to the Continent, with the Netherlands accounting for 40% of shipments, followed by France at 35% and Belgium at 24%. This trend of high demand from the continent increased significantly in March and April of this year following the announcement of the EU ban on imports of Russian petroleum products and the price cap. We expect the European energy needs to drive a steady increase in demand for tonne-miles for LR2 tankers from AG, which will support firmer freight rate dynamics in the second half of the year.

Today's volume of clean oil flows from the East destined for Western countries is having a positive impact on LR2 tanker size. As shown in image 5, we have seen months of consecutive increases in the monthly volume of tonnes from the ending of the first quarter 2022, with the LR2 tanker size grasping the lion share of business this year. March ended with a peak not seen before in the volume of clean flows from the East to West with a total nearing 5m tonnes, with MR tankers losing share of the business. In the months of January till April 2023, (image 5 right chart), LR2 tankers share is almost 60% compared to 20% share in the case of Panamax size, and 11% share for MR2.

Today's volume of clean oil from the East destined for Western countries has a positive impact on the size of LR2 tankers. As image 5 shows, monthly volumes have steadily increased and March ended with an unprecedented peak in clean flows from east to west, totaling nearly 5 million tonnes with MR tankers losing their share of the business. In January-April 2023 (image 5, right chart), the share of LR2 tankers was nearly 60% compared to 20% for Panamax tankers and 11% for MR2 tankers.

A look at vessel supply for Jubail, Saudi Arabia, with Max ETA 14 days ahead, image 6, shows that in April there was relatively low supply between the middle and end of the month, which caused market prices for LR2 AG to rise to levels of WS180 and above. However, in early May, the number of vessels jumped to 30 and above, reducing the previous firmness of LR2 rates. The recent increase in vessel supply fuels uncertainty about rate trends, although demand sentiment and clean oil flows offer optimistic potential for the outlook for LR2 market rates.

Latest AIS since: Maximum number of days from latest AIS received. Trade: This selection includes all vessels competing for cargoes in the selected trade: i. Vessels that are currently in this trade. ii. Vessels that are willing to compete for this trade. Market deployment: Market deployment based on Signal Ocean information. Market Rates: Market rates for the relevant route. Commercial Status: Commercial status of the vessel at each point in time. Max ETA: ETA window for available vessels to reach the loading port 14 days. Last 90 days: Number of days back (from today) to start the chart.

IV. Clean Demand Ton Miles

The optimistic outlook for the LR2 segment can be clearly seen in the year-over-year growth in tonne-miles (image 7), as the trend is consistently higher than in any month last year, while the MR clean segment shows a downward trend in May after peaking in February. At the end of the first quarter of the year, the challenge of substituting Russian oil products for LR2 tankers is developing positively with growth in tonne miles from all areas to all destinations.

The increase is even more surprising if we focus on the evolution of ton-miles for LR2 tankers from the area AG to Europe, while in the case of MR we still see a strong decrease, confirming the increasing share of employment for LR2 tankers from East to West. (image 8)

Looking ahead, it is a clear trend that exports from East to West will increase mainly due to LR2. Therefore, we maintain an optimistic outlook for LR2 market prices and a more conservative approach for MR, as growth in clean demand in ton-miles appears to be declining in the case of the MR size. The Arabian Gulf region will continue to play a critical role in substituting Russian petroleum products as demand on the continent leads ton-mile growth, while the United States is also a major destination for clean petroleum product exports from Saudi Arabia. It remains to be seen how clean freight rates will develop in the second half of the year and the extent to which Europe will continue to substitute Russian oil for clean petroleum products, as energy demand has increased more than in previous years. The clean tanker segment LR represents a size in terms of supply and demand that offers growth opportunities in the AG trade, while it remains to be seen whether the smaller clean tankers will gain strength from trading other light and medium clean oil products.

On July 30, the worlds largest 24000TEU container ship Ever Ace built by Samsung Heavy Industries for Evergreen Marine made its maiden voyage to Qingdao Port, Sh......

Evergreen Marine Corp. reportedly doled out year-end bonuses of as much as 40 months wages to some of its employees on Thursday. According to local media reports......

Duringthe process of using ECDIS installed onboard, there are lots of questions and doubts raised by the mariner, this may cause confuse when PSC inspection and ......

Seacon Marine Technical Pte ltd. is a professional maritime technology service company affiliated to Seacon Ships Management Co., Ltd. It has supervised the cons......

Deck machinery and systems of ships are continuously subjected to harsh weather and corrosive environment. Machinery such as cargo cranes and associated auxiliar......

This article contains crucial information regarding anchoring in Ningbo-Zhoushan VTS zone NO.1 and its nearby areas, providing clarification and guidance for int......

Pacific International Lines (PIL, the Group), today announced the Groups unaudited financial results for financial year 2019 (FY 2019) and first half 2020 (1H 20......

If you thought that with just an up-to-date engine room and a skilful crew you can set sail on your ship to high seas then you were wrong. A ship along with its ......

On November 2, 2020, Shanghai Shipping Exchange officially launched Shanghai (Export) Containerized Freight Index based on Settled Rates (SCFIS). SCFIS represent......

Commissioned by ourentrusting party, Guangzhou Shipping Exchange Co., Ltd. (GSE) determines to organize an online bidding for a bulk carrier named TIGER LIAONING......

.gif)

Image 4: Clean Oil Flows - East to West, by Destination Country https://app.signalocean.com/tanker/dynamic/oilflows

Image 4: Clean Oil Flows - East to West, by Destination Country https://app.signalocean.com/tanker/dynamic/oilflows Image 5: Clean oil Flows, (Saudi Arabia, UAE, China, India, Oman, Qatar) to West (U.S., U.K., NETH, Italy, France, Spain, Belgium), by Vessel Class https://app.signalocean.com/tanker/dynamic/oilflows

Image 5: Clean oil Flows, (Saudi Arabia, UAE, China, India, Oman, Qatar) to West (U.S., U.K., NETH, Italy, France, Spain, Belgium), by Vessel Class https://app.signalocean.com/tanker/dynamic/oilflows Image 7: Clean Demand Ton Miles, LR2 and MR tanker size class categories https://app.signalocean.com/tanker/reports/toncharts-trade

Image 7: Clean Demand Ton Miles, LR2 and MR tanker size class categories https://app.signalocean.com/tanker/reports/toncharts-trade Image 8: Clean Demand Ton Miles, AG to Europe https://app.signalocean.com/tanker/reports/toncharts-trade

Image 8: Clean Demand Ton Miles, AG to Europe https://app.signalocean.com/tanker/reports/toncharts-trade

Ningbo Containerized Freight Index Weekly Commentar

Ningbo Containerized Freight Index Weekly Commentar  Ningbo Containerized Freight Index Weekly Commentar

Ningbo Containerized Freight Index Weekly Commentar  BIMCO Shipping Number of the Week: Bulker newbuildi

BIMCO Shipping Number of the Week: Bulker newbuildi  Ningbo Containerized Freight Index Weekly Commentar

Ningbo Containerized Freight Index Weekly Commentar  Ningbo Containerized Freight Index Weekly Commentar

Ningbo Containerized Freight Index Weekly Commentar