The Asian low sulfur fuel oil market will enter 2022 on a firm footing that was likely to continue for much of the year due to the emergence of China as a major ship refueling destination.

The optimistic outlook comes despite concerns surrounding the potential for demand destruction by the fast-spreading COVID-19 omicron variant.

Even though the marine fuels sector has remained relatively more resilient to demand loss from pandemic restrictions than other transportation fuels, industry watchers have said that global demand was stymied by about 10% in 2020 and has only been limping back to near-normal in 2021.

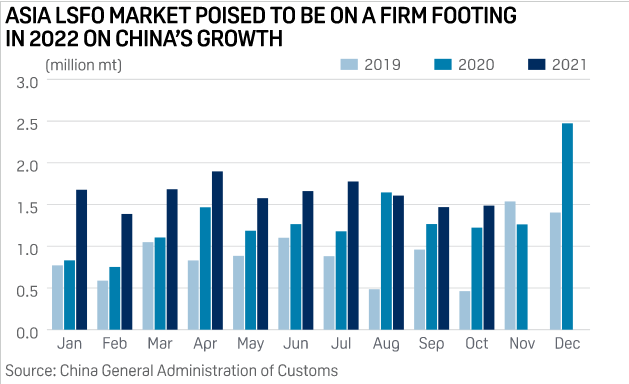

However China's fuel oil exports, which mainly comprise the sale of bonded bunker to ocean-going vessels, surged 42.91% year on year to 15.65 million mt in 2020, and at 16.22 million mt over January-October 2021 were up 36.1% year on year, latest General Administration of Customs data showed.

China's bonded bunker fuel market, which market sources estimate may finish 2021 at around 20 million mt, is expected to further expand in 2022. To help fuel this growth, Beijing is likely to increase fuel oil export quotas in 2022, market sources said. The government has issued 11.39 million mt of low sulfur fuel oil export quotas in 2021.

“The government will increase the export quota,” a fuel oil trader at a Chinese company said, adding that it would encourage further production ramp-up, thereby making product pricing increasingly competitive, especially compared with Singapore.

Competitive pricing

The production ramp-up by Chinese producers since early 2020 has led suppliers at Zhoushan, a major bunkering hub in Zhejiang province in China's east, to competitively price low sulfur bunker fuel to increase market share.

Zhoushan-delivered marine fuel 0.5%S bunker prices averaged $5.06/mt higher than the same grade delivered in Singapore in 2020, but as of Dec. 23, IMO-compliant product delivered at Zhoushan had traded at an average discount of 50 cents/mt to Singapore in 2021, S&P Global Platts data showed.

Furthermore, Beijing's move in late November to permit regional port authorities at Shanghai and Guangzhou to approve bunker suppliers themselves will likely lead to more suppliers entering the market and potentially increase price competition further, market sources said.

“More suppliers are expected to enter the market in the first half of 2022, making competition heat up,” another Shanghai-based trader said.

Singapore, the world's largest ship refueling destination, is likely to increasingly feel the heat due to rising competition, particularly from China, market sources said.

While sales of bunker fuel to ships calling the city-state rose 5% year on year to 49.83 million mt in 2020, traders estimate bunker sales in 2021 remain steady or only a touch higher due to increasing competition, especially from China. Singapore bunker sales over January-November 2021 stood at 45.81 million mt, latest Maritime and Ports Authority of Singapore data showed.

“Singapore's low sulfur bunker fuel volumes are expected to shrink in 2022 due to a slowdown in demand as neighboring ports continue to capture market share,” a Singapore-based trader at a Japanese trading company said.

China has the advantage of being able to ramp up LSFO production, so sustained growth looks imminent, and will likely be at the cost of Singapore losing some of its volumes, another Singapore-based fuel oil trader at a Western trading company said.

Supply tightness

The supply tightness that has characterized the upstream Singapore marine fuel 0.5%S cargo market for most of the fourth quarter in 2021 is expected to continue into early 2022, traders said.

Market sources estimate Western arbitrage LSFO volumes arriving in Singapore in Q4 at around 2 million mt/month and did not expect arrivals in January to be significantly higher, and perhaps lower than the 2.5 million mt/month of LSFO that typically lands in Singapore.

Valuations in the upstream Asian marine fuel 0.5%S cargo market are also likely to be held in good stead in early 2022 on expectations of incremental demand for LSFO as a burning fuel from the regional utility sector, traders said.

The optimistic outlook is reflected in the market structure of the Singapore marine fuel 0.5% swaps curve, which for the whole of 2022 is well backwardated.

More representative of a near-term outlook though is the fact that January-February and February-March swap spreads stood at double-digit backwardations of $18.30/mt and $11.25/mt respectively at the Asian close Dec. 23.

Source: Platts

The opinions expressed herein are the author's and not necessarily those of The Xinde Marine News.

Please Contact Us at:

media@xindemarine.com

.gif)

Ningbo Containerized Freight Index Weekly Commentar

Ningbo Containerized Freight Index Weekly Commentar  Ningbo Containerized Freight Index Weekly Commentar

Ningbo Containerized Freight Index Weekly Commentar  BIMCO Shipping Number of the Week: Bulker newbuildi

BIMCO Shipping Number of the Week: Bulker newbuildi  Ningbo Containerized Freight Index Weekly Commentar

Ningbo Containerized Freight Index Weekly Commentar  Ningbo Containerized Freight Index Weekly Commentar

Ningbo Containerized Freight Index Weekly Commentar