This is Part 1 of 5 in the S&P Global Platts Metals Trade Review series, where we dig through datasets and digest some of the key trends in metallurgical coal, iron ore, steel, scrap and alumina. We also explore what the next few months could bring, from supply and demand shifts, to new arbitrages, and to quality spread fluctuations.

Seaborne metallurgical coal and coke markets have entered 2021 in the wake of a transformative fourth quarter of 2020, which saw significant shifts in trade flows and price dislocations due to China’s temporary halt on Australian coal imports.

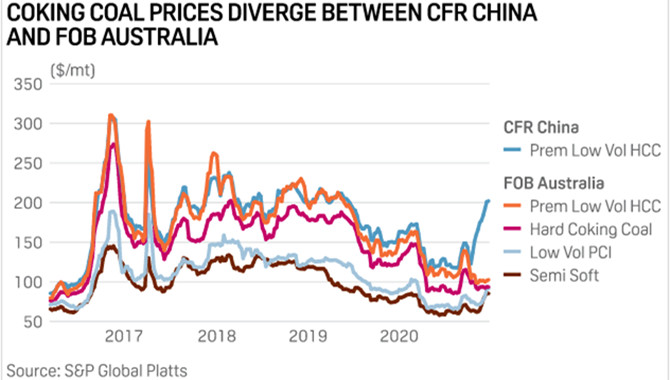

Premium low-volatile hard coking coal prices slumped 23% to $101.50/mt FOB Australia at end December from the quarter before, while prices on a CFR China basis surged 40% over the same period to $201/mt, S&P Global Platts data showed.

Such price dislocation was observed across all grades of metallurgical coal in Q4, with the bulk of Australian met coal spot trade flow shifting from China to other destinations, widening the price differential between the FOB and CFR China benchmarks.

China has previously relaxed its import quotas each January, but this year the market is less sure that Australian imports will resume, given the state of relations between the two countries. An optimistic view sees cargoes waiting at Chinese ports being allowed to unload before new bookings can be made for Australian met coal. The pessimistic view is that the ban, which was imposed in October, will be extended. The latter view seems more likely.

On the supply side, the impact of La Nina looks set to be less severe than previously envisaged. Australia’s Bureau of Meteorology has suggested the current La Nina is already approaching its peak, reducing the likelihood of any severe weather-related curtailment of coal exports from Queensland in the current quarter.

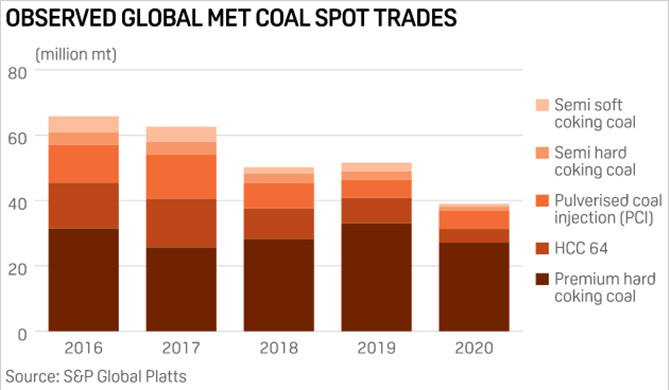

MET COAL SPOT TRANSACTIONS FALL 24%

Seaborne met coal spot trade volumes fell 24% year on year to 39 million mt in 2020. Platts observed a total of 514 spot transactions in the year, comprising premium, second-tier, semi-hard and semi-soft coking coal, along with pulverized coal injection coal used for steelmaking. The total does not include spot transactions for US exports.

This compares with 51.6 million mt of spot transactions observed by Platts in 2019, and is below the 55 million mt/year average over the past three years. Around 67% of all spot transactions observed in 2020 were for cargoes bound for China, with 33% going to other global markets. This compares with 79% and 21%, respectively, in 2019.

The sharp decrease in spot trades in 2020 reflects disrupted global steel markets due to the coronavirus pandemic, as well as China’s import halt on Australian coal reducing the overall trade flow. While China remained a primary importer in the year, a growing proportion of Australian coals were sold to ex-Chinese markets through Q4 2020 and early January.

With global steel markets continuing to recover from the pandemic, import demand from the “traditional” FOB markets has increased markedly. Spot transactions for premium hard coking coal from countries outside of China, including India and in Europe, surged 51% in Q4 from the previous quarter to 48 million mt.

India’s steel market recovery was reflected in stronger demand for metallurgical coke. The quarterly average for 64/62 CSR coke rose 18.9% quarter on quarter to $313.84/mt CFR India in Q4.

Meanwhile, Japan, a seller of seaborne met coke for much of 2020, has turned buyer again due to higher blast furnace utilization rates.

Notwithstanding the recovery in ex-China steel markets, most participants anticipate a continuing oversupply in the seaborne market in the current quarter. This could see Australian spot tonnage continue to seek homes outside of China, potentially putting pressure on the wider spot market.

The brand relativities of Australian coals exported to China sank in late Q4, while Platts premium low-volatile or PLV CFR China prices tracked higher.

Over October-December, Australian Peak Downs prices fell from 89% to 62% of the benchmark PLV CFR China price, while Goonyella prices fell from 83% to 58%.

As import restrictions show no signs of easing in early January, Chinese steelmakers have shown they are willing to pay for premium hard quality material from Canada and the US in light of domestic coking coal prices climbing 20% over Q4.

Market participants expect prices will rise in the current March quarter as demand for domestic coal is expected to increase in the absence of Australian imports.

Due to different coal preferences, the withdrawal of Chinese buyers and the emergence of ex-China demand has led to premium mid vol brands trading at a premium to Platts PLV FOB Australia. PMV cargoes typically trade at a discount to PLV, but steelmakers outside of China prefer higher fluidity of coals to support stronger steel output, resulting in PMV coals trading 1%-3% higher than PLV.

This situation is expected to persist until there is greater clarity on China’s coal import restrictions.

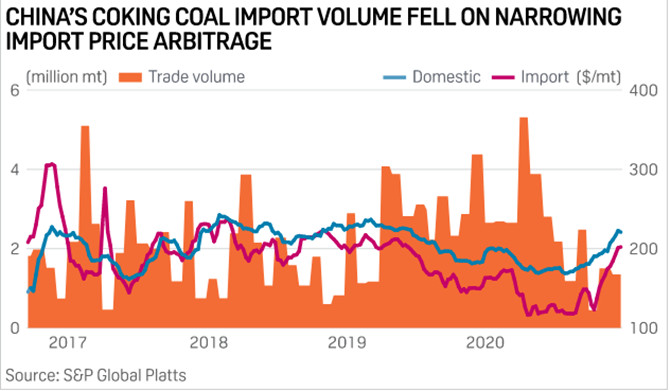

The arbitrage between domestic and imported coking coal prices in China is seen as a barometer of Chinese import demand, and the import price usually moves in line with the domestic coking coal market.

The import price arbitrage narrowed from $65.40/mt on Oct. 26 to $18.80/mt on Dec. 30, primarily driven by import prices, which were up $53.50/mt or 36% from the start of the quarter.

China’s domestic coking coal prices increased by 23.4% on quarter due to the import ban, as strong Chinese steel consumption in Q4 boosted demand for domestic coking coal and coke, both of which were in tight supply.

Source:Platts

The opinions expressed herein are the author's and not necessarily those of The Xinde Marine News.

Please Contact Us at:

media@xindemarine.com

.gif)

Ningbo Containerized Freight Index Weekly Commentar

Ningbo Containerized Freight Index Weekly Commentar  Ningbo Containerized Freight Index Weekly Commentar

Ningbo Containerized Freight Index Weekly Commentar  BIMCO Shipping Number of the Week: Bulker newbuildi

BIMCO Shipping Number of the Week: Bulker newbuildi  Ningbo Containerized Freight Index Weekly Commentar

Ningbo Containerized Freight Index Weekly Commentar  Ningbo Containerized Freight Index Weekly Commentar

Ningbo Containerized Freight Index Weekly Commentar