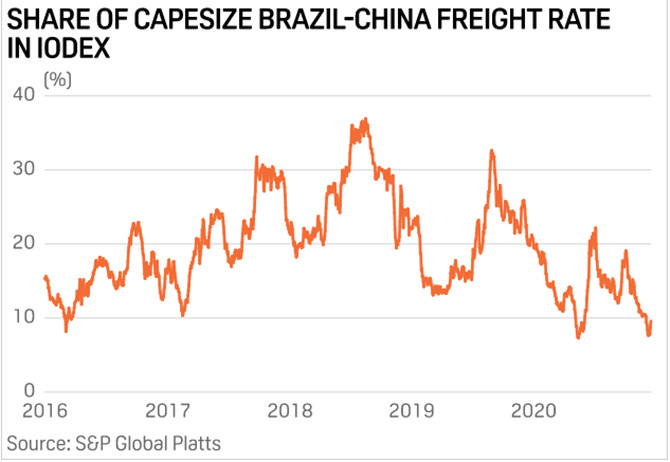

The Capesize freight rate as a percentage of the seaborne iron ore price has touched a record low, with a supply crunch for the mineral along with excess tonnage availability altering the correlation.

The share of the key Brazil to China Capesize freight rate in the benchmark S&P Global Platts IODEX 62% Fe CFR China index fell below 8% for the week ended Dec. 12 compared with the five-year average of about 20%.

A strong iron ore market has not really helped perk up Capesize freight rates. The Platts IODEX 62% CFR price has averaged $127.62/dmt in the fourth quarter compared with a year-to-date average of $106.38/dmt.

Close to 80% of iron ore cargoes are shipped on Capesizes.

The Platts Capesize Brazil to China 170,000 mt (plus/minus 10%) rate has averaged $15.51/wmt during the current quarter, while the year-to-date average has been $14.74/wmt.

“It’s [the current trend] because the freight market is being dragged down by the lack of coal cargoes this year, whilst iron ore trade is still doing very well,” said Ralph Leszczynski, research director of Genoa-based shipping consultancy Banchero Costa.

Strong sentiment in the iron ore market saw IODEX break the $160/dmt mark on Dec. 11, aided by healthy Chinese steel margins, a recovery of steel demand in Japan and Europe, as well as supply constraints from major iron ore exporting countries like Brazil and Australia due to operational and weather issues.

“The historical correlation is gone. High iron ore prices mean limited commodity supply, thus less transportation,” a Capesize shipowning source said.

While iron ore miners have all the incentive to maximize output, with iron ore prices in the $100-$120/dmt range, there was limited support for Capesize despite Western Australian producers operating at full capacity, a chartering source said.

The benchmark iron ore index touched a nine-year high at $160.70/dmt Dec. 11. The last time IODEX was higher was on Oct. 12, 2011, at $161.25/dmt.

Lack of coal cargoes

A lack of coal cargoes has impacted the Capesize market to an extent, which otherwise would have kept a reasonable volume of tonnage employed.

“Whilst on the other hand, coal demand has been a disaster this year; not because of any Chinese ban on Australian coal, but primarily due to a collapse in coal demand from Europe, South Korea and India,” said Leszczynski.

Capesize market participants have allayed fears of iron ore prices above $150/dmt triggering smaller shipments on Supramax, Panamax or Post-Panamax class bulkers, claiming such movements will be marginal.

However, a stream of newly built Valemax and Guaibamax type ships, which have entered the market this year, is eating into the share of the spot Capesize market. Iron ore volumes on Valemaxes and Guibamaxes will be at 106 million mt this year and are expected to increase 32% to 140 million mt next year, according Brazilian miner Vale.

Iron ore demand

Demand for iron ore is expected to remain firm in China and recover further in other regions, including Japan and Europe, with the restart of blast furnace capacity idled earlier this year due to the pandemic.

This will also see some iron ore supply drawn away from China back to their usual destinations, which could in turn help support Capesize freight rates.

Source: Platts

The opinions expressed herein are the author's and not necessarily those of The Xinde Marine News.

Please Contact Us at:

media@xindemarine.com

.gif)

Ningbo Containerized Freight Index Weekly Commentar

Ningbo Containerized Freight Index Weekly Commentar  Ningbo Containerized Freight Index Weekly Commentar

Ningbo Containerized Freight Index Weekly Commentar  BIMCO Shipping Number of the Week: Bulker newbuildi

BIMCO Shipping Number of the Week: Bulker newbuildi  Ningbo Containerized Freight Index Weekly Commentar

Ningbo Containerized Freight Index Weekly Commentar  Ningbo Containerized Freight Index Weekly Commentar

Ningbo Containerized Freight Index Weekly Commentar