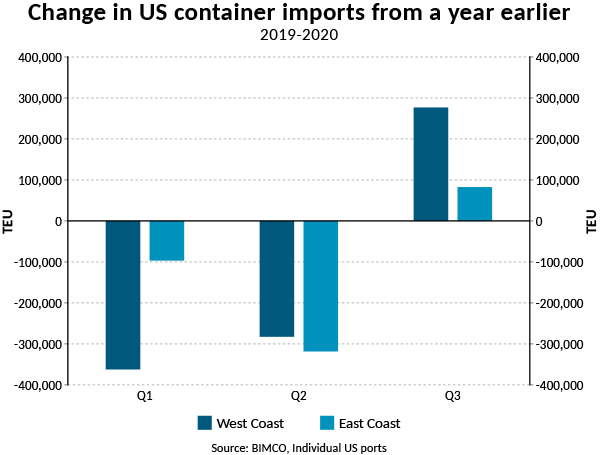

Over the first nine months of the year, the USWC is down by 4.4% and the USEC by 4.3%, compared with the same period of 2019. The USWC saw a much larger drop in the first quarter. It was hit hard by the factory closures/lockdowns in China, but has seen higher growth in the third quarter than the USEC, leaving them both with similar percentage drops.

The extra containers into the US in the third quarter of the year came primarily from the Far East, with volumes between here and North America in Q3 up 18.7% compared with Q3 2019. This was enough to bring accumulated exports over the first three quarters into positive territory for the first time in October, with year-on-year growth up 1.7%. The growth in this trade is not enough to make up for lost volumes elsewhere, which explains why total imports into the US are still down.

It is a different story when it comes to Far East to Europe trade, where accumulated volumes are still down 8.3% in the first nine months of this year compared with last. Part of the reason is that retail sales in the EU have been slower to recover than their American counterparts. Compared with September 2019, retail sales in the EU are up by 2.1%, while in the US, October sales rose by 8.6%.

Globally, the first nine months of the year have seen accumulated volumes fall by 3.4%. As expected, the third quarter has proven to be the strongest, and the only one posting year-on-year growth compared with 2019 (+1.2m TEU).

Strong volumes in recent months have sent freight rates soaring. On average in the first half of the fourth quarter, a 40-foot container from the Far East to the USWC cost shippers USD 3,844.7 dollars. Compared with the average in Q4 2019, this represents a 117% jump.

Smaller, yet still considerable, jumps can be seen between the Far East and the USEC and North Europe. Here spot freight rates by 16 November stand at USD 4,828 per TEU (up 99.9% from 16 November 2019) and USD 2436 per TEU (+69.9), respectively.

In mid-September, when spot rates into the US were already at record highs and still increasing, the Chinese government called a meeting with the major carriers for a discussion on capacity management and further General Rate Increases (GRIs). On 15 September, spot rates into the US jumped for the last time, though they remain at or near the record-breaking levels.

As spot freight rates were rising to new highs, long-term contract rates were initially unaffected, but the GRIs announced at the start of the October marked the first large jumps in contract rates for some time. In contrast, where the USWC has seen the largest jump, long-term contract rates into the USEC have risen by the most. Compared with 30 September, they are 30.6% higher at USD 3,242 per FEU. Long-term freight rates into the US rose 16.9% over the same period to USD 1,925 per FEU.

While freight rates have been rising, bunker fuel prices remain low, offering carriers even larger margins than the headline rates suggest, and assuring strong profits for the last quarter of this year.

Fleet news

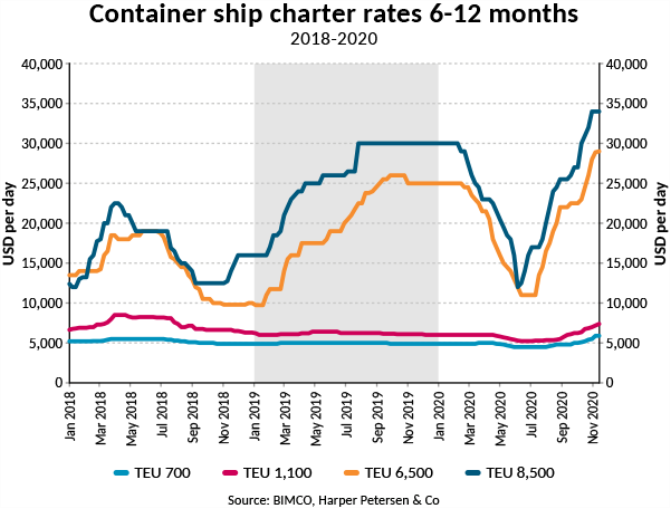

The closure of demolition yards coincided with the high idle fleet and low charter rates, and demolitions didn’t pick up in these months. The reopening of yards coincided with the recovery in demand for container ships, meaning owners considering demolition during the difficult months thought again and fixed their ships at profitable rates. Because of the current strength of the container market, BIMCO has revised its demolition forecast down by 100,000 TEU to 200,000 TEU.

So far this year, 93 ships have been demolished, removing 184,380 TEU from the market. The vast majority are feeder ships (76) with an average capacity of 1,343 TEU. The remainder comprises 7 post-Panamax ships (averaging 5,182 TEU) and 10 Panamax ships (4,441 TEU).

Counteracting demolitions, deliveries totalled 721,582 TEU, leaving fleet growth at 2.3% so far this year. BIMCO expects that by the end of the year the container shipping fleet will have reached 23.6 m TEU, a rise of 2.7% from the start of the year.

Looking further ahead, the orderbook paints a picture of how attractive different ship sizes are to owners. The most popular are feeder and ULCS, depending on which measure you choose. There are currently 182 feeder ships on order but, as they average only 1,735 TEU, the 52 ULCS on order account for the largest share of the order book by far when measured in DWT (1.1m DWT out of 2m). The decreasing popularity for newbuilt, mid-sized ships can be explained by the carriers’ continued focus on the economies of scale provided by the large ships, and the feeders needed to accommodate the hub and spoke model.

Outlook

This year has certainly turned out much better than expectations at the end of last year and in the immediate aftermath of the coronavirus outbreak. When volumes were down in the first half of the year, carriers managed to avoid freight rates crashing by lowering capacity offered, and once volumes started to rise, they were ready to reap the rewards of higher rates and lower bunker costs.<

However, even though the worst-case scenario has been avoided this year, the outlook remains clouded. The virus is still spreading at alarming speed, putting the recovery on hold, and once again shuttering many shops in major advanced countries.

Furthermore, the strong retail spending in the US can in large part be put down to the USD 1,200 payment to Americans and extra unemployment support. The effects of these are now running out, and although more stimulus is much needed, that is unlikely to come until the new administration takes over in late January.

What will happen when volumes start falling will depend on how carriers react. Will they return to their pre-pandemic ways – the often-low freight rates and what that entails? Or will they take with them the lessons learned from this year and focus less on market share and on capacity management instead? While this was very effective in the short term, it has yet to be seen whether it is a strategy that can hold in the longer term. Along with bunker prices, the idle fleet will be an important metric to watch for insight into carriers’ profitability.

The rise in long-term rates will ensure that carriers fixing contracts now will be somewhat insulated from the risk of rates dropping again if carriers fail to adjust capacity when volumes start falling.

The increase in rates also means carriers’ profitability is insured for a while longer, even if volumes do start to fall again. The vast majority of containers are fixed on long-term contracts and, if a carrier can fix considerable volumes for the next year at current long-term rates (Far East to USWC USD 1,905; to USEC, USD 3,227; and to Europe, USD 1,609 per TEU), their bottom lines will be more resistant to any future declines in spot rates.

The opinions expressed herein are the author's and not necessarily those of The Xinde Marine News.

Please Contact Us at:

media@xindemarine.com

.gif)

Ningbo Containerized Freight Index Weekly Commentar

Ningbo Containerized Freight Index Weekly Commentar  Ningbo Containerized Freight Index Weekly Commentar

Ningbo Containerized Freight Index Weekly Commentar  BIMCO Shipping Number of the Week: Bulker newbuildi

BIMCO Shipping Number of the Week: Bulker newbuildi  Ningbo Containerized Freight Index Weekly Commentar

Ningbo Containerized Freight Index Weekly Commentar  Ningbo Containerized Freight Index Weekly Commentar

Ningbo Containerized Freight Index Weekly Commentar