In an opinion piece on the company website, Navin Kumar, Director, Drewry Maritime Research says that after 2020, ships operating with scrubbers will enjoy a competitive advantage but that will reduce over time and may last for only a few years.

According to Kumar, Ever since the date of implementation of the regulation on bunker fuel by the IMO was declared, shipowners have been evaluating the pros and cons of fitting scrubbers. The two main questions haunting owners are:

Whether the price premium of the compliant fuel (VLSFO/MGO) over high sulphur fuel oil (HSFO) will be strong enough to recover the cost of scrubbers in time to justify the huge investment?

As most of the existing bunker demand shifts towards compliant bunker fuels, will bunker suppliers continue to supply HSFO to be used in scrubber-fitted vessels?

Kumar believes, the recent forecast by the International Energy Agency (IEA) eases the concerns of shipowners regarding the availability of HSFO. Despite the fact that a major chunk of the existing HSFO demand will shift towards the compliant fuel after the implementation of the new regulation, demand will still be strong enough to induce bunker suppliers at major ports to continue to offer HSFO.

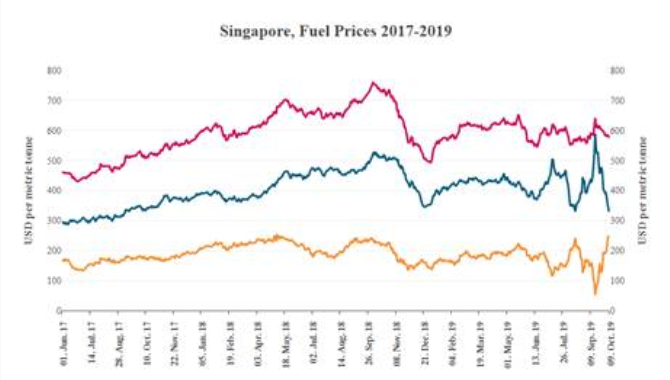

According to the IEA, demand for HSFO will decline from 3.5mbpd in 2019 to 1.4mbpd in 2020, and will further decline slightly to 1.1mbpd by 2022 with the improvement in VLSFO supply (3.5% sulphur). Nevertheless, during 2022-24, HSFO demand will be surprisingly resilient at around 1.1mbpd, as vessels fitted with scrubbers will support demand. According to the agency, more than 5,000 vessels will be fitted with scrubbers by end-2024.

Currently, about 11% of the global fleet (in terms of GT) is either scrubber-fitted or pending retrofit. At the same time, about one-third of the vessels in the orderbook will be fitted with scrubbers. The share of scrubber-fitted vessels (including pending retrofit) in large vessels, especially tankers and bulk carriers is high, due to their higher bunker consumption. While the share is more than 20% for large tankers (VLCCs and Suezmaxes), it is above 15% for Capesize bulkers, which suggests that bunker suppliers at ports handling these large bulk vessels will continue to supply HSFO.

Although there is still high uncertainty regarding the possible premium of LSFO over HSFO, the expected tight supply of the compliant fuels suggests that the premium will be strong enough to recover the cost of scrubbers within the first two years.

Kumar says, “We expect the average price premium of LSFO over HSFO to be around $240 per tonne in 2020, which will gradually decline to close to $80 per tonne by 2023 once the LSFO supply improves. As the premium in the price of compliant fuel will narrow significantly after the first two years, the business case for retrofitting scrubbers will disappear in later years.

Based on our bunker price forecast, a scrubber-fitted non-eco VLCC will earn around $12,500pd more than a non-eco VLCC without a scrubber in 2020. However, the earnings premium of scrubber-fitted VLCCs will decline to around $4,000 pd by 2023.

As LSFO will continue to hold the price premium of around $75 per tonne over HSFO even beyond 2023, scrubber-fitted vessels will continue to earn more than non-eco vessels without scrubbers. Moreover, non-eco scrubber-fitted vessels will be able to compete with modern eco-vessels (around 15% more fuel efficient) even beyond 2023.

Source:Drewry

The opinions expressed herein are the author's and not necessarily those of The Xinde Marine News.

Please Contact Us at:

admin@xindemarine.com

.gif)

Maersk to integrate Hamburg Süd and Sealand

Maersk to integrate Hamburg Süd and Sealand  Launch of the construction of the first Ro-Ro saili

Launch of the construction of the first Ro-Ro saili  Oil tanker explosion kills at least 3 in central Th

Oil tanker explosion kills at least 3 in central Th  Wind-powered RoRo Vessel Secures €9 Million in EU

Wind-powered RoRo Vessel Secures €9 Million in EU  London plays a pivotal role as shipping seeks to re

London plays a pivotal role as shipping seeks to re  Shell unveils five energy sector trends to watch in

Shell unveils five energy sector trends to watch in